Tuesday, February 23, 2010

Put Fannie and Freddie on budget

Today, U.S. Representative Michele Bachmann (MN-06) took part in a press conference as a cosponsor of the Accurate Accounting of Fannie and Freddie Mac Act. The bill is aimed at instituting a proper and complete accounting for the Government-Sponsored Enterprises Fannie Mae and Freddie Mac.The Obama Administration has been in the news this month with claims that Fannie and Freddie are not going to be that expensive. After projecting Treasury investments of $230 billion to prop up the two companies, the budget a few weeks ago said the investment would be $188 billion. Of that, about $97 billion is to be returned in dividends from the two firms by 2020. This does not count, alas, the $175 billion inserted into the firms by the Federal Reserve, nor the $1,250 billion of their debt -- mortgage-backed securities -- that the Fed has purchased. San Francisco Fed President Janet Yellen said yesterday that these purchases "were vital in preventing a complete financial breakdown," which might tell us Fan/Fred are still in some rough shape. I don't know that the legislation would count Fed contributions to Fan/Fred.

The Congressional Budget Office estimates that Fannie and Freddie added $291 billion to the federal deficit in 2009 and will cost an additional $389 billion to run over the next ten years. However, Fannie and Freddie are currently considered �off budget� meaning the actual cost to run these agencies is not considered by the Office of Management and Budget. By moving the activities of Fannie and Freddie Mac �on budget�, their financial obligations would then be included in the federal government�s budget and debt projections and provide a more accurate picture of our nation's precarious finances.

�The Accurate Accounting of Fannie Mae and Freddie Mac Act is a much needed remedy for a Washington that needs to come to terms with their spending addiction. One thing we know about Fannie and Freddie is that they cost the already overburdened and financially strapped taxpayer a pretty penny.

�Why should Fannie and Freddie be able to run up these numbers without the President having to reflect this risk in his budget? It just doesn�t make sense, and we owe it to the taxpayers to be transparent and forthcoming on the commitments we�re making with their credit card.�

Not to mention the fact that Fannie and Freddie are now paying off private debt holders of its MBS that are 120 days or more delinquent. It gets bad debt off the books of the two companies, but investors receiving this money are now getting money they cannot reinvest at the rates they used to get. Realizing the losses on those MBS will add to the cost of the bailout of these two firms -- it's worth remembering that the AIG bailout cost US taxpayers a relatively modest $9 billion.

Chief author of the legislation is Rep. Scott Garrett of New Jersey.

Labels: banking, economics, Michele Bachmann

Tuesday, January 26, 2010

Taxing banks so satisfying

We would prefer that the government convincingly precommit to a policy of not saving financial institutions that fail. However, given everything that has transpired in the past couple of years, such a policy announcement would be greeted by laughter. No one would believe it.Brian Wesbury and Robert Stein yesterday in their weekly outlook. This addresses the who decides question, but who is TBTF and what is the consequence? I think this is the important part of their proposal:

As a result, the key issue for policymakers is not whether some banks are too big to fail, but who bears the cost of this status. The best solution is to change the way banks are regulated so the burden of getting too big to fail is carried by the same stakeholders who allow the company to get that way in the first place. Some regulator, perhaps the Federal Reserve � which tends to be relatively more isolated from political pressure � should have the discretion to certify if a financial company gets too big to fail or �TBTF.�

If the Fed designates a company as TBTF then some pre-set extra regulations should be triggered to make sure the bank does not take excessive risk at taxpayer expense.

However, it is important to remember that every company should have a free choice about whether it wants to be in this position. Regulators would need to work with the banks to communicate when they are getting close to TBTF status, so banks know whether they are going to trigger this extra layer of regulation.It is interesting that the LA Times also editorialized on this point on Sunday.

One key problem with President Obama�s drive to tax bank liabilities is that it would apply to many companies that are not particularly large, signaling investors that maybe some midsized companies are now TBTF. In other words, it casts the net way too wide. Another problem is that it�s based on a desire to raise revenue lost because of past policy mistakes, when it should be focused on preventing future policy mistakes.

How many initiatives can President Obama justify by pointing to the public's outrage over excessive bank bonuses? Last week the administration called on Congress to tax big banks, insurance companies and brokers to recoup what taxpayers spent bailing out the financial markets. This week the administration added two more items to its legislative to-do list: a cap on the size of banks, and a ban on certain types of investing. Although an argument can be made for the proposals, they go further than necessary to protect taxpayers against the risk of future bailouts. And that's the real goal, even if it's less politically satisfying than hammering banks.But this administration's economic policy has never seemed to do anything that wasn't politically satisfying. At least when Bush wanted to do something satisfying he chose something hard like Social Security reform. Say what you will about the proposal, but populism was not in it. One has to wonder where this president would be if he didn't have "fat-cat bankers" to bash?

For a different take see Tom Cooley (h/t: Mankiw)

Friday, January 22, 2010

Bernanke a victim of Brown-mania?

Hard to believe, but the Bernanke reconfirmation may be in serious trouble. Ed Morrissey fleshes out the story. The stock market sags partly in response. The WSJ Market Beat blog has a roundup of economists' reactions. A current tally shows 17 votes for reconfirmation, 12 against (including five Democrats), with five more Democrats answering that they are at this time undecided. Many of the Democrat opponents, including Barbara Boxer and Russ Feingold, announced their opposition today. Majority Leader Reid and Minority Leader McConnell are now jointly counting noses to see if they have 60 votes (as the more anti-Fed types like Jim Bunning are placing a hold on Bernanke's nomination.)

Opposition to the Fed chair seems to have increased since the election of Scott Brown on Tuesday. The Huffington Post reports this afternoon that

We get this rather unprincipled announcement from Sen. Boxer:The election in Massachusetts has senators who previously considered themselves safe watching their backs, and they don't relish the prospect of a vote in favor of a man who failed to foresee the financial crisis and is closely associated with Wall Street.

A recent poll found that 47 percent of Americans think Bernanke cares more about Wall Street than Main Street, while only 20 percent think he works for Main Street. Independents, who swung heavily for Brown in Massachusetts, are even more opposed to Bernanke than Democrats or Republicans. Fifty percent of independents think he cares first about Wall Street; 15 percent think he prioritizes the needs of Main Street. That's a difficult vote in the face of an angry public.

If Bernanke is confirmed, he'll have to rely on the same coalition that moved the bailout through Congress, when the leadership of both parties joined forces to oppose the rank and file.

No, Senator, it is not the job of the Federal Reserve to be a champion for Main Street, Wall Street, or anyone else. The Federal Reserve is an independent institution, a feature that Congress chose wisely almost a century ago."I have a lot of respect for Federal Reserve Chairman Ben Bernanke. When the financial crisis hit in late 2008, he took some important steps to prevent what many economists believe could have been an even greater economic catastrophe," said Boxer.

"However, it is time for a change -- it is time for Main Street to have a champion at the Fed. Dr. Bernanke played a lead role in crafting the Bush administration's economic policies, which led to the current economic crisis. Our next Federal Reserve Chairman must represent a clean break from the failed policies of the past."

The Fed, as Robert Samuelson points out, has had officials testify before Congress 32 times. Its actions are not a secret, and attempts to find out who got direct loans from the Fed are more meant to intimidate than illuminate. The assault on its independence has helped push down stock prices and could set off a currency crisis in a G-7 currency, which is extraordinary. At a time where financial crisis still looms large in the rear view mirror, it is highly irresponsible to engage in scapegoating.First, central bank independence has been shown to be essential for controlling inflation. Sooner or later, the Fed will have to scale back its current unprecedented monetary accommodation. When the Federal Reserve judges it time to begin tightening monetary conditions, it must be allowed to do so without interference. Second, lender of last resort decisions should not be politicized.

Finally, calls to alter the structure or personnel selection of the Federal Reserve System easily could backfire by raising inflation expectations and borrowing costs and dimming prospects for recovery. The democratic legitimacy of the Federal Reserve System is well established by its legal mandate and by the existing appointments process. Frequent communication with the public and testimony before Congress ensure Fed accountability.

Overnight, every senator realized the quickest, easiest way to populist street cred is to treat Bernanke like he's the third Salahi.

Labels: banking, economics, Federal Reserve, money

Friday, January 15, 2010

Tomorrow on the King Banaian Show

Labels: banking, economics, KYCR, Media, NARN

Thursday, January 14, 2010

Greed is like gravity

What the law professors propose is interesting -- a personal liability for bank debts created by paying in assessable stock. As Pedro would say, incentives matter, and making bank CEO income dependent on not taking too many risks would help. But I would wonder how to handle banks that gamble over time -- assessable stock would either have to be restricted to not sell for several years or you lose the stick that keeps the incentive in place. But which bankers would accept the loss of income from being assessed for bank mistakes that could happen after that banker moves on? I haven't read all of their paper, but it is an intriguing idea.A popular answer to the question [Why Are Bankers Reckless?] above based on political populism and inept moralism is: "because they're greedy." As an explanation it's as sophomoric as saying that airplanes crash because of the force of gravity, but apparently it gets some people elected.University of Minnesota law professors Hill and Painter came with a better explanation based on sound economics: "because of wrong incentives created by poorly designed government regulations."

Tuesday, December 15, 2009

Best sentence I read today

Instead, if you think in terms of "how can we optimally regulate so that banks have only incentives to do great things and no incentives to take excess risk," you are on the wrong track.From Arnold Kling, who argues that if you cannot imagine a world without deposit insurance -- and he doesn't -- then you have to have a world without big banks. Our experience with private deposit insurance so far has been miserable, as the fate of state deposit insurance funds in the S&L crisis made clear. Nobody has deep enough pockets. If banks can constantly game the system once they hit a certain size, perhaps you just can't let them be that size.

Simon Johnson seems to think you can just cut out all the bad things banks can do and make them just do the unrisky stuff. But didn't we try that with Glass-Steagall? How do we really think we can put the genie back in that bottle?

Wish I had time to think more about this, but grading continues for hopefully only another 24 hours. More when I can. In the meantime, please read back on "the regulatory dialectic".

P.S. I was going to give this to Alex Tabarrok's post on setting a carbon tax that varies by temperature when I started writing it this morning. Worth your time.

Thursday, November 05, 2009

Congress played health care fiddle while housing burned

A much-anticipated audit of the Federal Housing Administration was abruptly postponed just before it was supposed to be made public, after questions arose about its accuracy.Sure a bad time for this, particularly given Barney Frank's continuing headache with Fannie Mae.

The auditor, Integrated Financial Engineering, said it notified the F.H.A. late Tuesday that its computer models were creating unexplained inconsistencies. A news conference scheduled for Wednesday morning was canceled.

The delay came amid broad public concern about the financial condition of the F.H.A., and appeared likely to add to questions about whether the agency is running excessive risks with taxpayers� money.

Fannie Mae reported a net loss of $18.9 billion in the third quarter of 2009, compared with a loss of $14.8 billion in the second quarter of 2009. ... Third-quarter results were largely due to $22.0 billion of credit related expenses, reflecting the continued build of the company�s combined loss reserves and fair value losses associated with the increasing number of loans that were acquired from mortgage backed securities trusts in order to pursue loan modifications.Yup, another $15 billion going into Fannie to bail out the housing industry. Congress' answer? Keep more first-time homebuyer credits flowing. Damn the pusher man.

...

As a result, on November 4, 2009, the Acting Director of the Federal Housing Finance Agency (FHFA) submitted a request for $15.0 billion from Treasury on the company�s behalf.

Labels: banking, economics, housing

Tuesday, October 27, 2009

Can FDIC solve "too big to fail" for non-banks?

I agree with this -- in fact, did last month -- but it has been clear for awhile that the Fed didn't want this role. In fact, the college of regulators is a Bernanke idea from a few weeks ago. You might argue Bernanke was just seeing the handwriting on the wall, but I doubt many in the Fed disagree with Vincent Reinhart's appraisal.Under this authority, jokingly referred to as "Death Panels for Banks," the Federal Deposit Insurance Corp. would oversee the dismantling of large financial firms much as it does now when it intervenes in commercial banks that are at risk of insolvency.

Decisions about which institutions are so large that they pose a system-wide risk and must be monitored would be made by a Council of Regulators, comprised of leaders from the Fed, the Treasury Department, the FDIC, and other bank-oversight agencies.

...Some independent analysts also have warned that handing the Fed new, expansive powers as the systemic risk regulator could distract it from its principal role of setting monetary policy to sustain growth and contain inflation."I didn't want the Fed to have that role because I think monetary policy is too important," said Vincent Reinhart, a former top Fed economist who's also wary of the emerging legislation. "If all you do is a college of regulators, that's just inviting a debating society."

Reinhart and Fed governor Dan Tarullo have both argued in the last week that the problem is too-big-to-fail and that the issue is how to deal with non-bank financial giants like Lehman and AIG, for which regulators had to improvise. (See the McKinley and Gegenheimer timeline FMI.) If these companies are going to be placed under some government protection in a too-big-to-fail environment, I have to disagree with Ed that they don't get some kind of regulation. You may own a skyscraper as your private property, but when you tear it down you're responsible for any damage done to nearby buildings. If a private non-bank fails and in the process takes down healthy financial institutions that were counterparties, you may have a reason for using the law to limit collateral damage. (That doesn't mean you always get it right, as John Carney points out in the AIG case.)

So what can be done, if we're not going to use the Fed or FDIC? Before you say "we have to do something", consider the benefits of large banks, says Charles Calomiris. Diversification, economies of scope and extended reach to developing markets are some of these benefits. Are we at risk of losing those gains as we try to solve too big to fail?

UPDATE: John Taylor summarizes the testimony around Frank's FDIC proposal.

Labels: banking, economics, Federal Reserve

Monday, October 05, 2009

The Minnesota dollar

Leslie Davis, a candidate for governor (who received 1% of the votes of delegates in a straw poll last weekend at the state GOP convention) proposes that we

...pass a law requiring Minnesota state--chartered-banks to create debt-free checkbook-money and use it to build a state-of-the-art transportation system of roads, rails, bridges and ports. And maintain them. This will create thousands of jobs, begin paying the debt out of the system, This is not a loan, it is simply a new legally required service of state-chartered banks.But this made no sense to me, because for the bank to create money it must create a liability on its balance sheet. What is the offsetting asset you put on the books to keep your balance sheet in balance, or what do you reduce in your liabilities or net worth?

So I had to rummage around a bit but apparently this idea was in a bill last year proposed by a bipartisan set of sponsors (including local GOP representative Dan Severson.) SF 705 proposes just what Mr. Davis wants. In relevant part,

Subd. 3. Origination and movement of project money. (a) The commissioner of management and budget shall notify all state-chartered banks of the project number and its total bid value. The bid value must be divided among all state-chartered banks in proportion to their capital and surplus as of the due date of their financial reports submitted to the commissioner of commerce under section 48.48, for the most recent reporting period that ended at least 90 days before the date of notification to the state-chartered banks regarding that project. Using the accepted ability of banks to create money, each state-chartered bank shall create money equal to its share of the bid value of each project.So this means that the amount of reserves a bank holds to keep your deposits safe would be drawn down by the state.

(b) Each state-chartered bank shall then electronically transfer this money to the commissioner of management and budget.

(c) The commissioner of management and budget shall then electronically transfer this money as payment under the terms of the project contract into a checking account maintained by the contractor in a state-chartered bank. The commissioner shall make the payments only at the direction of the governmental agency for which the project is performed.

Subd. 4. Direction to bank examiners. The state-chartered banks are free of any

reserve requirements affected by the creation of money required under this section; this money is deemed to be an asset to the state-chartered bank, to the state, and to the people of this state, and not as a liability to anyone.

Ellen Hodgson Brown wrote about SF705 last year, but it argues that the deposits must go on the books as an asset. This is wrong, however. A bank cannot create an asset without creating a liability -- balance sheets must balance. A comparable scheme was invented in Guernsey in the 19th Century, but the bank received a note from the state to hold as the asset. Perhaps this is meant by the bill when the Commissioner of Management and Budget divides up the bid values of projects. But that would be an unsecured debt; how would FDIC treat this?

Guernsey is a well-known haven for offshore banking, and site of some of the Icelandic banking crisis' collateral damage. And we should note that Guernsey uses its own currency. I am unclear how this is to work if the banks of Minnesota are still to use a unified U.S. dollar. Brown suggests that this act may be unconstitutional. There was private money between the end of the Second Bank of the United States in 1836 and the National Bank Act of 1863. (I own several examples of that private money.) But short of creating a Minnesota dollar, I do not see how this could work other than placing on the asset side of state-run bank a non-interest-bearing promissory note from the state government. To me that looks like a tax on bank earnings, and would quickly encourage most state-chartered banks to seek a national charter.

Labels: banking, economics, Minnesota

Monday, September 14, 2009

Fixing what you can't see

The Wall Street Journal, at least, has taken notice.

Vern's documents are all published at Scribd. The feds, of course, would like to get a judge to simply throw out these cases, but Judicial Watch is currently on this case.Last December, Mr. McKinley sent a FOIA request to the Fed to find out what Fed governors meant when they said a Bear Stearns failure would cause a "contagion." This term was used in the publicly-released minutes of the Fed meeting at which the central bank discussed plans by the Federal Reserve Bank of New York to finance Bear's sale to J.P. Morgan Chase. The minutes contained only the vague warning of doom, without any detail on how exactly the fall of Bear would destroy America. Mr. McKinley's request sought the supporting documents for this conclusion.

He also requested minutes of the autumn FDIC board meeting at which regulators approved financing for a Citigroup takeover of Wachovia. To provide this assistance, the board had to invoke the "systemic risk" exception in the Federal Deposit Insurance Act, and therefore had to assert that such assistance was necessary for the health of the financial system. Yet days later, Wachovia cut a better deal to sell itself to Wells Fargo, instead of Citi. So how necessary was the FDIC's offer of assistance?

After Mr. McKinley sued the agency this summer, the FDIC coughed up a previously undisclosed staff memo to the FDIC board. Again, the agency redacted the substance, providing roughly two pages of text from the nine-page original. The section of the memo titled "Systemic Risk" was entirely erased. As for the Fed, it blew off Mr. McKinely's initial request and has since responded mainly with some highly uninformative letters from the Fed staff to Congress.

Many of FDIC's actions are relatively routine. Its closure over this weekend of $7 billion Corus Bank of Chicago, however, contains a "private placement" of $4 billion of Corus assets. How private is this? Who is the purchaser, and how many bids are there? One would think this is public information. Researchers like Vern are simply interested in writing the history of this unique moment in international finance.

The WSJ concludes:

A public debate on which banks really needed a bailout via the government's AIG conduit has hardly taken place. And did all of Bear Stearns' creditors, including hedge funds, need to be made whole to ensure the survival of American capitalism?A year after the epic meltdown, this is the debate Congress needs to undertake before legislating any new federal authority. Regulators should not receive a blank check to prevent systemic risk without even defining what that term means.

Labels: banking, Federal Reserve

Monday, August 31, 2009

Ownership society, TARP edition

- Government forces banks to take capital injections. Government gets warrants to buy common stock in the process.

- Government tells banks how to operate.

- Banks want government out, make an offer to buy their shares and warrants away.

- Banks raise private capital, pay off the government.

- Government declares victory.

Is this a good thing?

It occurs to me that this "earned a return for the taxpayers" line is becoming the Leviathan equivalent to those annoying "it's for the children" appeals on TV. It obviates any need to really think about what was done in the first place. If earning a return for taxpayers was a criterion for government performance, let's put the whole portfolio up in Morningstar and see how many stars our elected officials earn?

Labels: banking, economics, Obama

Thursday, August 27, 2009

The cupboard is Bair

That second paragraph is important -- they don't just have $10.4 billion, but also a reserve fund, which the FDIC places at $32 billion. And FDIC has a line of credit with the Treasury for $100 billion on which it can draw, though FDIC Chair Sheila Bair says they do not expect to draw on the line.The U.S. has taken over 81 banks this year, including Guaranty Financial Group Inc. in Texas and Colonial BancGroup Inc. in Alabama, amid the worst financial crisis since the Great Depression. The surge forced regulators to charge banks an emergency fee to raise $5.6 billion for its insurance fund, which fell to $10.4 billion as of June 30 from $13 billion in the previous quarter, the agency said. The total was the lowest since the savings-and-loan crisis in 1993....

An $11.6 billion increase in loss provisions for bank failures caused the decline in the reserve fund, the FDIC said. If the fund is drained, the FDIC has the option of tapping a line of credit at the Treasury Department that Congress extended in May to $100 billion, with temporary borrowing authority of $500 billion through 2010.

Worth noting: The Midsummer Review we discussed Tuesday included the return of $250 billion from the financial market backstop. Perhaps they've moved money away prematurely.

In the meantime, Richmond Federal Reserve president Jeffrey Lacker is sounding hawkish again.

The Federal Reserve may not need to buy the full $1.25 trillion in mortgage-backed securities the central bank has authorized by year-end as the economy improves, ...�I will be evaluating carefully whether we need or want the additional stimulus that purchasing the full amount authorized under our agency mortgage-backed securities purchase program would provide,� Lacker said today in a speech in Danville, Virginia.

Lacker has said the central bank should avoid favoring specific credit markets such as mortgages and consumer loans and instead boost the money supply with more �neutral� purchases of Treasuries. He cast the lone dissenting vote in January against the Federal Open Market Committee�s commitment to continue buying agency debt and mortgage-backed securities. In 2006 he dissented four times in favor of higher interest rates.

As the Fed continues to debate an exit strategy, more Fed presidents and governors will begin to look at this view. The fight is on for how soon exiting begins; as they move, look for more banks to fail.

Tuesday, July 14, 2009

Is everyone too big to fail?

A collapse would ripple across the �small and medium-sized businesses who rely on CIT to operate -- to pay their vendors, ship goods to their customers and make their payroll,� the New York-based lender said in internal documents obtained by Bloomberg News that make the case for its importance to the U.S. economy. CIT spokesman Curt Ritter declined to comment on the documents.The proper course of action here will be to find a merger (they've hired a reputable law firm to assist already) and for the government to monitor the situation but not interfere. It would sound confidence in the financial system and would be a win for the Geithner Treasury. But alas it appears Treasury is pushing the panic button, mindful that it bailed out GMAC. Of course, the latter has ties to a new union-owned business. So if you hear today someone from the Congressional Black Caucus speaking about CIT and minority owners, you'll have found the connection they are making to get the same political deal GMAC did.

CIT executives spoke with regulators during the past two days, according to a person familiar with the talks, after its bonds and shares tumbled on concern that the Federal Deposit Insurance Corp. won�t allow the lender into its bond-guarantee program created last year to unfreeze debt markets.

It appears that it's FDIC and Ms Bair that are arguing for tough love, at least according to John Carney. I'm in the middle of House of Cards right now, and the similarities to the Bear Stearns collapse -- the markdown of credit ratings, the drying up of short-term lending to CIT -- are scarily familiar. And they point up once again the problems of the current regulatory regime that Minneapolis Fed President Gary Stern pointed up in a recent speech. (Square brackets indicate where I've spelled out abbreviations Stern uses.)

Just as we should not rely exclusively, or excessively, on [supervision and regulation], I do not think that imposing an FDICIA-type resolution regime on systemically important nonbank financial institutions will correct as much of the TBTF ["too-big-to-fail"] problem as some observers anticipate. To be sure, society will be better off if policymakers create a resolution framework more tailored to large financial institutions, in particular one that allows operating the firms outside of a commercial bankruptcy regime once they have been deemed insolvent. This regime would take the central bank out of rescuing and, as far as the public is concerned, �running� firms like AIG. That is a substantial benefit. And this regime does make it easier to impose losses on uninsured creditors if policymakers desire that outcome.Wasn't the Geithner Treasury supposed to have come up with a solution to all this? The cost of delay is rising. And since it appears Geithner has pushed Bair and other TBTF worriers aside, hang the cost of this next bailout squarely on the Obama Administration.

But I am skeptical that this regime will actually lead to greater imposition of losses on these creditors in practice. Indeed, we wrote our book precisely because we did not think that FDICIA put creditors at banks viewed as TBTF at sufficient risk of loss. We thought that when push came to shove, policymakers would invoke the systemic risk exception and support creditors well beyond what a least-cost test would dictate. We thought this outcome would occur because policymakers view such support as an effective way to limit spillovers. I don�t think a new resolution regime will eliminate those spillovers (or at least not the preponderance of them), and so I expect that a new regime will not, by itself, put an end to the support we have seen over the last 20 months.

UPDATE: Simon Johnson wonders if campaign contributions had anything to do with it:

You're only too big to fail if you pay.The decision therefore largely comes down to the administration. On this front, the lack of strong connections between CIT�s CEO and senior Treasury officials looks like a weakness. CIT seems to sit at the edge of the charmed circle, with regard to meetings, shared social engagements, and intellectual entanglements. This is a close call, but I think it is just on the outside of the circle � in the sense that with the overall financial market situation more stable, the GM bankruptcy well-managed relative to expectations, and other credit support programs still in place, the balance of official opinion will tilt against CIT.

So then it all comes down to political donations. At least in terms of what is in the public record, Mr. Peek has not been overly generous, but he did give money to John McCain � and not to any Democrats. If this is in fact the limit of his recent contributions, I think you know the outcome.

Wednesday, June 17, 2009

First look at bank reform -- not impressed

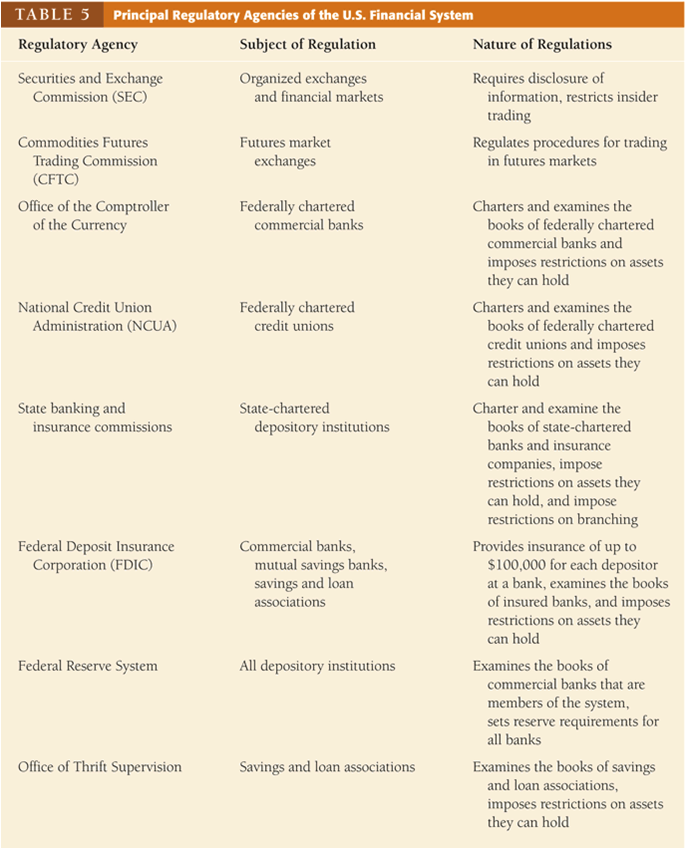

Above (please click to enlarge) is Table 5 from Chapter 2 of Frederic Mishkin's The Economics of Money, Banking and Financial Markets, 8th edition.* It maps for you the variety of regulators currently in the U.S. banking system. There's an interesting passage in the book much later on regarding multiple regulatory agencies:

Above (please click to enlarge) is Table 5 from Chapter 2 of Frederic Mishkin's The Economics of Money, Banking and Financial Markets, 8th edition.* It maps for you the variety of regulators currently in the U.S. banking system. There's an interesting passage in the book much later on regarding multiple regulatory agencies:Commercial bank regulation in the United States has developed into a crazy quilt of multiple regulatory agencies with overlapping jurisdictions. The Office of the Comptroller of the Currency has the primary supervisory responsibility for the 1,850 national banks which own more than half of the assets in the commercial banking system. The Federal Reserve and the state banking authorities have join primary responsibility for the 900 state banks that are members of the Federal Reserve System. The Fed also has regulatory responsibility over companies that own one or more banks (called "bank holding companies") and secondary responsibility for the national banks. The FDIC and the state banking authorities jointly supervise the 4,800 state banks that have FDIC insurance but are not members of the Federal Reserve System. The state banking authorities have sole jurisdiction over the fewer than 500 state banks without FDIC insurance. (Such banks hold less than 0.2% of the deposits in the commercial banking system.)That last bit is amusing (Mishkin has a new edition out next month, and I can't wait to see what he does with that second paragraph now!) So as we look at the new draft from the White House, what do we see? In their words (p. 2)

If you find the U.S. bank regulatory system confusing, imagine how confusing it is for the banks, which have to deal with multiple regulatory agencies. Several proposals have been raised by the U.S. Treasury to rectify this situation by centralizing the regulation of all depository institutions under one independent agency. However, none of these proposal has been successful in Congress, and whether there will be regulatory consolidation in the future is highly uncertain. (pp. 249-50)

- A new Financial Services Oversight Council of prudential regulators to identify emerging systemic risks and improve interagency cooperation.

- New authority for the Federal Reserve to supervise all firms that could pose a threat to financial stability, even those that do not own banks.

- Stronger capital and other prudential standards for all financial firms, and even higher standards for large, interconnected firms.

- A new National Bank Supervisor to supervise all federally chartered banks.

- Elimination of the federal thrift charter and other loopholes that allowed some depository institutions to avoid bank holding company regulation by the Federal Reserve.

- The registration of advisers of all hedge funds and other private pools of capital with the SEC.

It will take days to read and digest what's in there. For example, I'm quite concerned about the reduction in Federal Reserve independence that is reflected in the proposal (on p. 14) to force the Fed to get a signature from the Secretary of the Treasury before it could invoke its emergency powers (under Section 13(3) of the Federal Reserve Act) to prevent a financial crisis. I'm sure there are other little noxious nuggets among the 85 pages in this thing.

Let me make two points though. First, I showed the structure above and the quote from Mishkin to point out that most of us have thought the regulatory system was, if anything, too unwieldy. We were hoping for simplification. At first reading this proposal drops one regulator (the Office of Thrift Supervision, within FDIC) but puts two in its place, one for consumer finance protection and one for insurance firms. That just feels like it's going in the wrong direction, based on what we've taught in money and banking for the 25+ years I've done it.

Second, I fully agree with Arnold Kling that the Fed does see systemic fragility of the financial system as within its purview. I wrote several weeks ago that the Fed has basically two modes of conduct: in normal mode it fights inflation (with some eye on "high employment" as its goals insist -- the degree to which it looks at that varies by Fed chairman); in emergency mode it will act as a lender of last resort without regard to inflation in the short run. I am not yet sure there's any discussion in this draft of the connection between regulation and lending of last resort, or the connection between each of those and deposit insurance. (See Kahn and Santos [2005] for more.)

Kling also notes the Treasury brief is mute on housing policy. Can't imagine why.

*See also this from the Federal Reserve.

Labels: banking, economics, Federal Reserve, housing

Friday, June 12, 2009

Massive

European governments have approved $5.3 trillion of aid, more than the annual gross domestic product of Germany, to support banks during the credit crunch, according to a European Union document.

The U.K. pledged 781.2 billion euros ($1.1 trillion) to restore confidence in its lenders, the most of any of the 27 EU members, according to a May 26 document prepared by officials from the European Commission, the European Central Bank and member states and obtained by Bloomberg News. Denmark, where 13 of the country�s 140 banks were bailed out by the central bank or bought by rivals last year, committed 593.9 billion euros.

...The U.S. government and the Federal Reserve had spent, lent or committed $12.8 trillion, an amount that approaches the value of everything produced in the country last year, as of March 31.

A majority of new member states including Slovakia, the Czech Republic, Estonia and Lithuania have not taken public measures to support their financial markets, the draft said. Many banks in the region are foreign-owned. More than 80 percent of bank loans in central and eastern Europe come from lenders owned by six western European EU countries, according to Moody�s Investors Service.

Friday, May 29, 2009

Keep yer britches on: Nobody's replacing the dollar standard (yet)

Warning signs abound. Earlier this month, the Treasury discovered that demand had significantly decreased for its long-term bonds. In order to get buyers at its regular auction � the device by which the United States runs on deficit spending � it had to hike the interest rates it pays the bondholders. It signaled a lack of confidence in America's ability to sustain its debt expansion, which has the effect of worsening it through heavier debt service payments on the bonds they managed to sell.Now to be fair, Ed explains back on HotAir that "I allowed my imagination to run" and "I like to engage in a little speculative thinking," and that's great. I suppose I've done some of that on this blog. �But it's worth kicking the tires on this idea to understand what happened and why.

That reinforcing cycle of cascading debt has analysts worried enough to openly discuss downgrading U.S. debt. Financial Times reported this week that Standard and Poor has already done that for Great Britain's foreign debt, issuing a �negative� rating that will require more generous interest terms in order to sell bonds in international markets. The same kind of deficit spending in the United States will eventually trigger a re-evaluation of the U.S. credit, as the United States and United Kingdom face similar debt spirals with no end in sight.

Looking at the 12m change actually understates the swing in central bank demand. In the first quarter of 09, the outstanding stock of longer-term Treasuries rose by $278 billion. Central banks � according to the Treasury data � only bought $25 billion of longer-term Treasuries (all in March, and likely mostly short-term notes). China only bought $15 billion (all in March). Over that time period, central banks bought $85 billion in short-term Treasury bills, including $32 billion from China.

Labels: banking, economics, Federal Reserve

Thursday, May 28, 2009

Understanding MN bank reports

Return on assets, though, fell in Minnesota to 0.56% from 1.18% a year ago. Yields on loans are falling faster than their cost of funds, which is squeezing profits somewhat, and then you add to it larger charge-offs (for the uninitiated: a bank puts money aside in anticipation of losses on loans that are deteriorating; it then draws on that fund if the loan defaults as anticipated.)

The quality of loans held by Minnesota�s banks continued to decline. Net charge-offs as a percentage of total loans and leases were .94 percent, compared to .74 percent in the fourth quarter of 2008 and .48 percent in the first quarter of last year. Noncurrent loans and loans as a percentage of total loans and leases was nearly 3 percent, compared to 2.6 percent in the fourth quarter of 2008 and 1.5 percent in the first quarter of last year.Total loans of Minnesota banks fell from $80 billion a year ago to $54 billion now (deposits fell much less, from $62b to $56b.) The share of assets that were mortgages fell from 42% to 21% in the period. Equity capital has fallen from $8.2 to $7.1 billion in the same time.

This isn't bad, and it certainly isn't WaMu bad. But it isn't good for Minnesota when loans at its banks decline by a third. (That's different than saying credit in Minnesota declined by a third -- many of us get credit from institutions in other states.)

What is interesting about this period is that we have had only 8 commercial banks close, so many banks are restructuring while their leverage ratios have not moved very much. It appears that, as much as anything, the banks are going through this process in an orderly fashion. Bloomberg reports as well that banks' riskiness is now being better perceived by other market participants, so that weak banks are being charged higher rates than healthier ones. This is improving credit conditions:

U.S. companies have sold a record $600 billion of bonds so far this year, up from about $500 billion in the same period of 2007, according to data compiled by Bloomberg. Rates on 30-year fixed mortgages are about 1.8 percentage points more than 10- year Treasuries, down from 3.27 percentage points in December. ...And if all this talk about green shoots doesn't pan out... perish the thought.

While financial markets are improving, more than 60 U.S. financial institutions have collapsed over the past two years, according to Bloomberg data. In its latest quarterly survey of senior loan officers, the Fed found that more than 70 percent of respondents said bad loans will rise should the economy progress �in line with consensus forecasts.�

Labels: banking, economics, Minnesota

Monday, May 11, 2009

Let's review

A little humor to end the day. We had wondered if they curved the test, and it turns out the answer is "yes".

Friday, April 24, 2009

The cost of TARP

TCF Financial Corporation announced Wednesday that it had completed the repurchase of its TARP preferred stock from the U.S. Treasury. It paid a redemption price of $361.2 million plus accrued dividends of $3.4 million.Contemplate that last sentence: The government required TCF to drop its dividend in order to repay its loan. Would a bank be allowed to make you drop your kid's allowance from $5 a week to $1 before you could pay off the auto loan early? Banks in trouble often end up in agreements with the Fed that include seeking permission to pay any dividends, but banks were brought into TARP as a matter of solidarity, even patriotism. Solidarity isn't free, I guess.

TCF Chairman and CEO William A. Cooper said the bank had maintained a strong capital position over the last year through its own operations, and it didn�t need to rely on the public capital infusion to continue its traditional lending pace. Cooper said TCF is the largest bank to pay back TARP funds to the U.S. Treasury.

TCF�s executives had complained that Treasury and the U.S. Congress had subverted the TARP program by changing its rules after banks had joined. Those rules added controls over compensation and dividends programs, and Cooper said those changes contributed to a stigma of weakness and reliance on public support � a stigma that didn�t reflect his bank�s condition.

As part of the agreement for withdrawing from the program, TCF also agreed to reduce its first-quarter dividend from 25 cents to 5 cents.

How many pints of blood will be taken from the others?

U.S. banks that get preliminary results today of U.S. government stress tests may struggle to raise money after bad assets at the biggest lenders almost tripled on average in the past year.Emphasis added.Pittsburgh-based PNC Financial Services Group Inc. saw nonperforming assets -- those no longer accruing interest -- jump more than fivefold in the first quarter from a year earlier. They more than quadrupled at U.S. Bancorp in Minneapolis. At 13 of the largest U.S. banks, bad assets increased 169 percent on average from a year ago, according to first-quarter data compiled by Bloomberg.

The tests on the 19 largest banks are likely to focus in part on loan quality as a measure of health. The lenders, which may need to raise $1 trillion in capital to cushion losses according to an April 23 KBW Inc. report, may have a hard time persuading investors to give them cash.

...

If the banks learn the results of the stress [tests] today, �it�s a week plus until we find out, that�s where the danger is,� said Anton Schutz, president of Mendon Capital Advisors Corp. in Rochester, New York, which manages $150 million of financial stocks. Schutz runs the best-performing financial stock mutual fund over the past year, Burnham Financial Industries. �You get market movement on what might be fact or fiction,� he said.

Even if banks say their capital levels are adequate, the government could require them to raise more money, JPMorgan Chase & Co. Chief Executive Officer Jamie Dimon said April 16 during the firm�s earnings conference call.

�I don�t know what we need to do because it may not be solely up to us,� Dimon, 53, said in response to a question about whether the firm was planning to issue new equity. �I don�t think we need it.�

Thursday, April 23, 2009

A paper for my reading list

The turmoil after the Lehman Brothers failure is not so much an argument for intervention in that case, but rather an indicator of the impossibility of implementing a clear bright-line rule for bailouts. Efforts to distinguish a bright line between Bear Stearns and Lehman Brothers, and the lack of a consistent policy coupled with the multiple efforts to address the crisis, contributed to the angst visited upon market participants during 2008 and 2009. Even with the economic analysis resources at its disposal, the Federal Reserve has been unable to reliably predict contagion or judge an appropriate timing or level of intervention. Like the FDIC, the Federal Reserve has also been opaque with regard to the precise institution-specific reasons for intervention, which is seemingly at odds with Chairman Bernanke�s historical emphasis on transparency regarding central bank policy.I read a draft of this paper that Vern sent, and liked the focus on "clear evidence of contagion" for bailouts. (I think he and I agree less on whether there was clear evidence last September, but clarifying the criteria is useful.) It is not, as they say in the introduction,

...that the failure of an institution will impose losses on a broad array of creditors, shareholders, and counterparties, or that it will present a challenging or difficult receivership or bankruptcy process to work through. Even if a standard can be articulated, it is another matter to successfully implement that standard in practice. We believe that the lack of a clear standard and the shifting efforts at implementation have exacerbated the current financial turmoil by sending confusing and inconsistent signals to market participants.There is still the problem of convincing angry taxpayers and their supporters on Capitol Hill that contagion is a clear and present danger (if it does exist.) Those that try tend to get no thanks for their efforts, but I would prefer that those who see contagion work harder to make the case than telling the naysayers like Malkin to just shut up. As McKinley and Gegenheimer argue, that case isn't easy even for experts.

As I get closer to teaching money and banking next month, I'll focus on more of these papers. This one will be on the course reading list, which I will post (I'm in fact going to replicate my 2005 intro to econ series -- example -- with the lectures from this one -- this time maybe with sound and video??) Suggestions for additional readings invited in comments.

Tuesday, April 14, 2009

Letting the other team pay the umps

(BTW, there's a rather PG-13 rated slide show that made the rounds last fall to be found here.)

One of the places where I expect blame to be laid, complete with Barney Frank auto-da-fe, is the ratings agencies. Bloomburg's Caroline Baum, commenting on the failure thus far of the TALF program to jump-start credit markets, makes the point:

Most investors have neither the time nor the temperament to pick through individual loans that are pooled, sliced, diced and transformed into something with a credit rating and a cash flow to determine their viability. That job was designated to three credit-rating companies -- Moody�s Investors Service, Standard & Poor�s and Fitch -- which were paid by the issuer of the securities, not the investor.I wasn't aware of that history, and now want to know why we changed to having the issuer pay. Were investors just being cheap? Aren't they smart enough to understand the incentive incompatibility? It just seems very strange. It's like going to Yankee Stadium and letting the New York team hire the umpires because you don't want to pay for plane tickets for a third party arbiter.

That wasn�t always the case, according to Paul Kasriel, chief economist at the Northern Trust Corp. in Chicago. Prior to the 1970s, the onus was on the investor to pay for ratings.

That relationship removes the conflicts of interest inherent in the current system. Investors should be the one paying for credit evaluation, Kasriel says. �They�re getting a free ride.�

They also got what they paid for.

I just did not see how ratings agencies were any more able to determine the quality of a CDO-squared than a relatively sophisticated investor.

Also, I learned from the talk that AIG's chief regulator is the New York State Insurance Department. Is there any reason to believe that they had particular knowledge to evaluate the riskiness of AIG's financial products division? I read this on that site by the state insurance commissioner, a Mr. Eric Dinallo.

The fear in 2000 was that if we regulated credit default swaps and required holding sufficient capital, the market would go where unregulated sellers could make more money. We forgot that the biggest competitive advantage of the US financial system has always been safety, security and transparency. If we destroy that perception, the long-term cost to our society is incalculable.We're paying that cost now because rather than allowing the risky business to run offshore we decided we could rely on someone else to tell us where the risks are. It wasn't just investors outsourcing risk evaluation -- government did too.

Wednesday, March 25, 2009

Love this metaphor

Regulation is a chess mid-game, not a math problem. With a math problem, once you solve the problem, it stays solved. In a chess mid-game, new opportunities and threats arise constantly. You try to plan ahead, but your plans inevitably degrade over time.From the ever-quotable Arnold Kling. Anything that combines two passions like that for me -- though I have lost my chess playing as Littlest has grown out of it -- is a winner. It's a nice way to describe the regulatory dialectic.

Labels: banking, chess, economics

Tuesday, March 24, 2009

Maiden lane

That $29 billion was an investment vehicle called Maiden Lane. A Scholarly A for those of you who can, without Google, tell me who was funded by Maiden Lane II and Maiden Lane III.``The Federal Reserve has judged it necessary to take actions that extend to the very edge of its lawful and implied powers, transcending in the process certain long-embedded central banking principles and practices,'' Volcker said in a speech to the Economic Club of New York.

Fed Chairman Ben S. Bernanke last month agreed to lend against Bear Stearns securities, paving the way for JPMorgan Chase & Co. to buy its Wall Street rival. Bernanke, who worked with Treasury Secretary Henry Paulson to broker the bailout, last week defended the move as necessary to prevent ``severe'' damage to financial markets.

Volcker, the Fed chairman from 1979 to 1987, had implicit criticism for U.S. regulators and market participants who allowed ``excesses of subprime mortgages'' to spread into ``the mother of all crises.'' The Fed's Bear Stearns loan was unusual, he said.

``What appears to be in substance a direct transfer of mortgage and mortgage-backed securities of questionable pedigree from an investment bank to the Federal Reserve seems to test the time-honored central bank mantra in time of crisis: lend freely at high rates against good collateral; test it to the point of no return,'' he said.

...``The extension of lending directly to non-banking financial institutions -- while under the authority of nominally `temporary' emergency powers -- will surely be interpreted as an implied promise of similar action in times of future turmoil,'

Give up? Hint: the answer requires three letters. It's in the paper a lot these days.

I'm reading through the history of the Banking Act of 1933. I landed on a Cato Journal article by William Shughart, explaining the Glass-Steagall provisions in something other than the omniscient regulator perspective. Seems to follow what I'm reading as well in Charles Ellis' The Partnership.

Wednesday, March 18, 2009

Best sentence I read today

C'mon. If suicide were a proper penalty for piddling away taxpayer dollars, the National Mall would look just like Jonestown after refreshments.-- David Harsanyi (h/t: Russ Roberts)

UPDATE: This is almost as good:

I go back to Art Laffer�s four prosperity killers: inflation, higher tax rates, re-regulation, and trade protectionism. You can put a check mark next to each box.Yup.

Tuesday, March 17, 2009

What happened last time we tried this

More pressure has ensued, and now we have congresspersons contemplating a 100% tax on the bonuses. I'm not even sure that Mr. Liddy in sackcloth and ashes will slake the thirst for vengeance over payment on these contracts.

It is worth recalling however, as a reader wrote me today, that we have been here before. The Clinton Administration in its 1993 tax law change wanted to cap the amount of executive pay that could be deducted against income taxes. My correspondent writes:

There was also a loophole, a provision that said that Bonus Compensation was taxed differently than standard compensation. Bonus compensation under those provisions is fully deductible. That was the year when people like Michael Eisner of Disney got large bonuses for performance. Over time, Executive Compensation was shifted from Salary to Bonuses, and such provisions were written into Executive Contracts and those of other high performing employees. Presumably �Bonus Compensation� was to be tied to performance or certainly used as an incentive to get a star performer to move into a failing area of the business to help �right the ship�. Another point that is sometimes missed is that compensating someone with a bonus is being more responsible to the shareholders because this allows the company to structure its tote sheet in a way to reduce the overall corporate tax burden.I think in fact they get it. One person reported to me that a client of his, who works for a large firm, was asked to move as a division president of a part of the firm that was struggling. The compensation agreement called for base salary and bonus, and that the bonus was to be as a minimum equal to base salary. That minimum was what the fellow received for two years; he got more in year three as the division turned around.

Now fast forward to the �Banking Crisis� and �Bailout Packages� and we have a sudden attack on �Bonus Payouts�. People who apparently don�t understand how business works or how to get top level performers to stick their careers out on the line are attacking people who get such rewards.

A couple years ago, as Democrats were taking office, Business Week discussed the distortion in the structure of compensation induced by the Clinton tax policy.

Bill Clinton had what he thought was a great idea to curb the soaring paychecks of the nation's executives. It was 1991, shortly after the launch of his Presidential campaign, and he had just read a best seller on corporate greed by compensation guru Graef Crystal.

Clinton's brainstorm: Use the tax code to curb excessive pay. Companies at the time were allowed to deduct all compensation to top executives. Clinton wanted to permit companies to write off amounts over $1 million only if executives hit specified performance goals. He called Crystal for his thoughts. "Utterly stupid," the consultant says he told the future President.

"We were trying to shame companies into changing their behavior," says former Clinton senior adviser Bruce Reed. "And companies have been shameless in ignoring what we did." Or perhaps just astute in exploiting the flimsiness of Section 162(m) of the IRS code, as the measure is formally known. Reed acknowledges that the Clinton team deliberately watered down the proposal to make it more palatable by, for example, not applying the performance requirement to the award of stock options.

This is part and parcel of a process we've referred to for years as "the regulatory dialectic." Often the dialectical process is technological in nature, and other times it's provided intentionally by the process, as it was in 1993. The underpayment of base salary was induced, in no small part, by previous fits of populist pique against executive compensation, and now that it produces an undesired outcome -- "bonuses" for executives at failing firms that aren't really bonuses at all. So now we'll respond with some new law hastily written and barely passable as not a bill of attainder, and what will happen? Probably something unexpected, and at some time in the future undesirable. Rinse and repeat.

Labels: banking, economics, politics

Monday, March 16, 2009

The return of Regulation Q?

A better idea, even Warren Buffet seems to agree, might be to halt the visible taxpayer handouts on the banks' asset side. Let the massive guarantees already in place on the banks' liability side do the work of bailing out the system via the fat spreads banks are now earning above their government-guaranteed cost of funds. The advantage: It's relatively invisible and/or can be claimed that it's being done for the good of depositors, not bankers.From Holman Jenkins in this morning's Political Diary (subscription required.) One hopes this does not mean a restriction on competition for deposits; our experience with Regulation Q and the savings and loan debacle should be instructive. I think it instead will mean the continued provision of cheap credit via the Fed; Bernanke said last night as much.

Mr. Bernanke's TV appearance obviously took place with approval from the White House...I don't know how Jenkins knows that, but if so it's distressing to see Chairman Bernanke toss away the Fed's independence quite so blatantly. Cooperating is one thing, seeking approval is quite another.

Labels: banking, economics, Federal Reserve

Thursday, March 12, 2009

Mortgage for profit: everyone does it

Ed objects to the policy not because of Islamic principles at all but that the state is intruding into the private market. Sorry to say, Ed, that horse left the barn a very long time ago, with mortgage deductibility, Fan/Fred, CRA, etc.

The story has spread quite a bit. Yesterday James Taranto wondered if the users of these contracts had deprived themselves of a benefit:

Since mortgage interest is tax-deductible and principal is not, one assumes this means that borrowers with Islamic mortgages end up paying considerably more for the same house than those with regular mortgages. (The AP does not answer this obvious question.) If the law provided for an equivalent tax break for Islamic mortgages, however, presumably Shariah would permit Muslims to take advantage of it, since the ban is on interest, not tax advantages.I think that misses Ed's point though. If you give a deduction for interest on home mortgages you've handed a tax benefit for those who negotiate contracts that use interest to compensate lenders. An Islamic bank is compensated for the use of funds via marked-up principal. If that profit is not tax-deductible to the homebuyer, a dollar paid in mark-up is more costly than a dollar paid in interest, and the Islamic bank will face a lower demand curve for mortgages. Since the state has already intervened through the mortgage interest deduction, there's not much ground to stand on to say the state should abjure from supporting an Islamic mortgage instrument.

But what supports the use of Islamic mortgage instruments is, to go back to my hobby horse of the week, is a set of institutions that make banks comfortable with such an instrument. Virginia Postrel a few years ago interviewed Timur Kuran, a USC professor who has written the best one book on Islamic economics that I have read, Islam and Mammon: The Economic Predicaments of Islamism

Kuran warns that sometimes the purposes of Islamic banks goes beyond the creation of these contracts, though.

Islamic economists not only want their own banks, Professor Kuran writes. They ''desire new regulations that would force all banks to limit themselves to variable earnings and commitments.''But that's simply rent-seeking behavior, and that's not unique to Islamic banks.''And they want interest-based banking outlawed.''

Tuesday, March 10, 2009

Trust and bank policy

I think that key determinant in this [recession] is the degree to which Americans generally trust each other. That level has been sufficient to support democracy in the English-speaking world or Anglosphere. I'm more optimistic that our culture and moral fiber maintains trust even when confidence is shaken as it surely has been the last 18 months. To the extent it does, this recession shall pass, and like Shiller I'm not inclined to think stimulus does anything to shake that.Craig Newmark notes that the topic of trust has taken off lately. Since I wrote, Sapienza and Zingales have started to research the amount of trust in financial systems. Showing that it has declined, they conclude:

For financial markets to play their vital role once again, we must restore people�s faith in them. The most effective way to do so is to eradicate the perception that the government is run in Wall Street�s interest. The ethics rules issued by President Obama are a good but insufficient first step. More important is to redesign the bank rescue plan so that it clearly acts in the interest of the country (having well-capitalized banks), not the interest of Wall Street (having taxpayers bail out current investors).Newmark also links this paper by Bruce Yandle, which I've skimmed so far and think needs a full read. Trust is built through market transactions over time; formal rules help reduce that time. Describing Hayek's work he says:

Simply put, in the absence of market-generated trust-forming devices transacting parties could never afford enough police and regulators to induce honest behavior among ordinary people. Trust and trust-forming mechanisms can be a low-cost substitute for police, regulators and court actions.So what arises instead are, Yandle states, common codes and customs and certification, like audited balance sheets. Moody's and Standard and Poor's replaces a handshake. Willem Buiter goes further, saying "for every good, service or financial instrument that plays a role in your �model of the world�, you should explain why a market for it exists," since without some kind of trust only a "pre-Friday Robinson Crusoe autarky" exists.

Nothing said by the Obama Administration so far proposes to repair that. If anything, its silence on the banking system indicates it too has lost trust. (See this by Simon Johnson, e.g.) It is stuck having itself instead lampooned. (h/t: Greg Mankiw.)

Labels: banking, economics, Obama

Thursday, March 05, 2009

A quick question for economists and finance professors

Tuesday, February 10, 2009

Vaporware as bank regulatory policy

vaporware, n., New software that has been announced or marketed but has not been produced. ... Software that is not yet in production, but the announced delivery date has long since passed.Today Treasury Secretary Geithner went to Congress and unveiled the long-awaited plan, from the guy who's so smart that we can just ignore tax laws. What did we get from him? Transparency, which means we get a new website. What's on it?

This site is coming soon.Sort of like "the check's in the mail", eh, Mr. Geithner?

At the bottom of that page, however, there's a link to a seven-page pdf that actually smells like a plan. A comprehensive stress test, it says. A stress test means creating some relatively rare scenario or scenarios, and then doing a valuation model of the bank under those scenarios. They've been part of the Basel II framework for years. What does comprehensive mean, though? And it's not like we knew what the next crisis would be. Comprehensive might only mean all banks (over $100 billion of assets). I am not sure.

It's not clear from the document whether the regulators will do a full inspection of all the banks (like FDR in 1933).

Then I find this: While Geithner's statement says a public-private partnership, it looks like the capital fund comes from the government alone:

While banks will be encouraged to access private markets to raise any additional capital needed to establish this buffer, a financial institution that has undergone a comprehensive �stress test� will have access to a Treasury provided �capital buffer� to help absorb losses and serve as a bridge to receiving increased private capital. While most banks have strong capital positions, the Financial Stability Trust will provide a capital buffer that will: Operate as a form of �contingent equity� to ensure firms the capital strength to preserve or increase lending in a worse than expected economic downturn. Firms will receive a preferred security investment from Treasury in convertible securities that they can convert into common equity if needed to preserve lending in a worse-than-expected economic environment. This convertible preferred security will carry a dividend to be specified later and a conversion price set at a modest discount from the prevailing level of the institution�s stock price as of February 9, 2009. Banking institutions with consolidated assets below $100 billion will also be eligible to obtain capital from the CAP after a supervisory review.

That appears in some way to be a continuation of the Paulson Plan of recapitalization and then, as Jim Hamilton says, hope for the best. This is not impressing economists.

Worse, there's very little in the way of clarity on the public-private investment fund (p. 3 of the fact sheet), and an apparently close relationship with the Fed. �Hamilton makes the point:

The Treasury is acting as though there's a sixth party who can step into the funding gap here in the form of the Federal Reserve. Once again, that will be OK if Plan A works out, that is, if things go well enough that the Fed's losses on any assets acquired and loans extended are limited to the TARP funds already authorized. But if not, we're back to the same calculation-- the Treasury must borrow (if foreigners remain willing) and taxpayers must ultimately pay the bill. Either that, or the Fed just covers the bill by printing money for the whole thing.The result is that all we have is vaporware -- a forthcoming multi-trillion-dollar product that has been marketed but not delivered. ("Marketed"? Yes. "...tomorrow my Treasury Secretary, Tim Geithner, will be announcing some very clear and specific plans for how we are going to start loosening up credit once again.") �Mark Thoma:

Geithner's attempt at reassurance, that they're not quite sure how the program will work, or if they will get it right, but be assured that they are determined to keep tinkering with the program until it does work, has just the opposite effect. It undermines confidence. Why not wait until they actually have a plan before going public?Because the boss said jump.

Labels: banking, economics, Obama