Wednesday, June 17, 2009

First look at bank reform -- not impressed

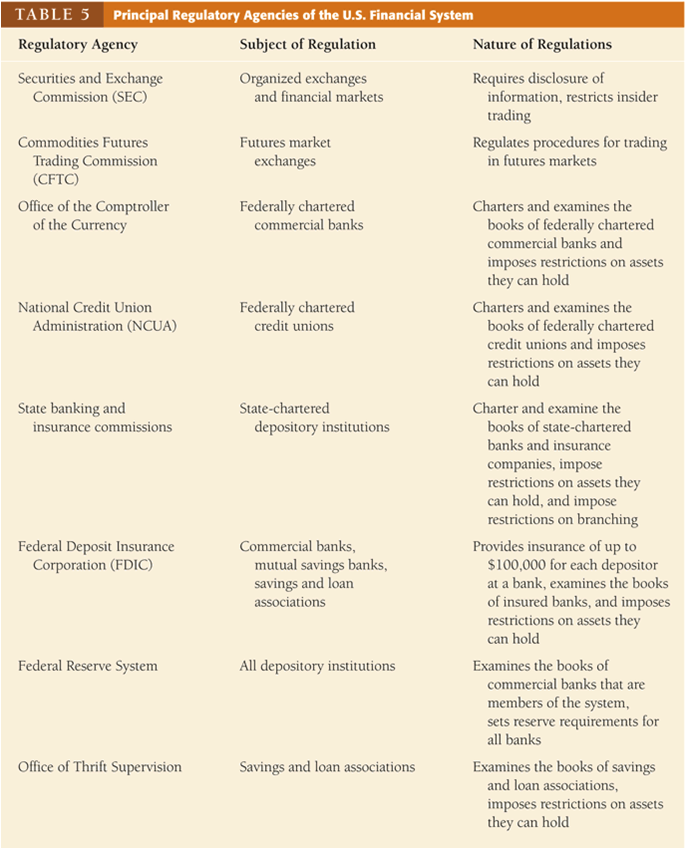

Above (please click to enlarge) is Table 5 from Chapter 2 of Frederic Mishkin's The Economics of Money, Banking and Financial Markets, 8th edition.* It maps for you the variety of regulators currently in the U.S. banking system. There's an interesting passage in the book much later on regarding multiple regulatory agencies:

Above (please click to enlarge) is Table 5 from Chapter 2 of Frederic Mishkin's The Economics of Money, Banking and Financial Markets, 8th edition.* It maps for you the variety of regulators currently in the U.S. banking system. There's an interesting passage in the book much later on regarding multiple regulatory agencies:Commercial bank regulation in the United States has developed into a crazy quilt of multiple regulatory agencies with overlapping jurisdictions. The Office of the Comptroller of the Currency has the primary supervisory responsibility for the 1,850 national banks which own more than half of the assets in the commercial banking system. The Federal Reserve and the state banking authorities have join primary responsibility for the 900 state banks that are members of the Federal Reserve System. The Fed also has regulatory responsibility over companies that own one or more banks (called "bank holding companies") and secondary responsibility for the national banks. The FDIC and the state banking authorities jointly supervise the 4,800 state banks that have FDIC insurance but are not members of the Federal Reserve System. The state banking authorities have sole jurisdiction over the fewer than 500 state banks without FDIC insurance. (Such banks hold less than 0.2% of the deposits in the commercial banking system.)That last bit is amusing (Mishkin has a new edition out next month, and I can't wait to see what he does with that second paragraph now!) So as we look at the new draft from the White House, what do we see? In their words (p. 2)

If you find the U.S. bank regulatory system confusing, imagine how confusing it is for the banks, which have to deal with multiple regulatory agencies. Several proposals have been raised by the U.S. Treasury to rectify this situation by centralizing the regulation of all depository institutions under one independent agency. However, none of these proposal has been successful in Congress, and whether there will be regulatory consolidation in the future is highly uncertain. (pp. 249-50)

- A new Financial Services Oversight Council of prudential regulators to identify emerging systemic risks and improve interagency cooperation.

- New authority for the Federal Reserve to supervise all firms that could pose a threat to financial stability, even those that do not own banks.

- Stronger capital and other prudential standards for all financial firms, and even higher standards for large, interconnected firms.

- A new National Bank Supervisor to supervise all federally chartered banks.

- Elimination of the federal thrift charter and other loopholes that allowed some depository institutions to avoid bank holding company regulation by the Federal Reserve.

- The registration of advisers of all hedge funds and other private pools of capital with the SEC.

It will take days to read and digest what's in there. For example, I'm quite concerned about the reduction in Federal Reserve independence that is reflected in the proposal (on p. 14) to force the Fed to get a signature from the Secretary of the Treasury before it could invoke its emergency powers (under Section 13(3) of the Federal Reserve Act) to prevent a financial crisis. I'm sure there are other little noxious nuggets among the 85 pages in this thing.

Let me make two points though. First, I showed the structure above and the quote from Mishkin to point out that most of us have thought the regulatory system was, if anything, too unwieldy. We were hoping for simplification. At first reading this proposal drops one regulator (the Office of Thrift Supervision, within FDIC) but puts two in its place, one for consumer finance protection and one for insurance firms. That just feels like it's going in the wrong direction, based on what we've taught in money and banking for the 25+ years I've done it.

Second, I fully agree with Arnold Kling that the Fed does see systemic fragility of the financial system as within its purview. I wrote several weeks ago that the Fed has basically two modes of conduct: in normal mode it fights inflation (with some eye on "high employment" as its goals insist -- the degree to which it looks at that varies by Fed chairman); in emergency mode it will act as a lender of last resort without regard to inflation in the short run. I am not yet sure there's any discussion in this draft of the connection between regulation and lending of last resort, or the connection between each of those and deposit insurance. (See Kahn and Santos [2005] for more.)

Kling also notes the Treasury brief is mute on housing policy. Can't imagine why.

*See also this from the Federal Reserve.

Labels: banking, economics, Federal Reserve, housing