Tuesday, February 23, 2010

Mopping up

Treasury anticipates that the balance in the Treasury's Supplementary Financing Account will increase from its current level of $5 billion to $200 billion. This will restore the SFP back to the level maintained between February and September 2009.This action will be completed over the next two months in the form of eight $25 billion, 56-day SFP bills. Starting tomorrow, SFP auctions will be held each Wednesday...

The purpose of this will be to provide a temporary draining of excess reserves from banks, replacing them with these relatively short notes. The Treasury doesn't keep the cash; it hoards it in the Fed's balance sheet (see item 33 here) until it the paper matures, then it repays it. At last report the banks held $1,119 billion in excess reserves, so this is not that big an adjustment. But if interest rates don't move very much over the next two months from tighter credit, it will be a sign that banks are not seeing great lending opportunities outside of Treasuries. And it will give us some indicator of what happens when the Fed starts issuing its own paper instead of needing Treasury's help.

(h/t: Donald Marron, who reminds us that the Treasury can only do this while it has room under the debt limit.)

Labels: economics, Federal Reserve

Monday, February 15, 2010

History may repeat

In this paper we provide some evidence on when central banks have shifted from expansionary to contractionary monetary policy after a recession has ended--the exit strategy. We examine the relationship between the timing of changes in several instruments of monetary policy and the timing of changes of selected real macro aggregates and price level (inflation) variables across U.S. business cycles from 1920-2007. We find, based on historical narratives, descriptive evidence and econometric analysis, that in the 1920s and the 1950s the Fed would generally tighten when the price level turned up. By contrast, since 1960 the Fed has generally tightened when unemployment peaked and this tightening often occurred after inflation began to rise. The Fed is often too late to prevent inflation.Michael Bordo and John Landon-Lane, in a new NBER working paper (ungated copy here.) Since September 23rd's FOMC statement the Fed has been emphasizing "resource utilization" and "resource slack", code for unemployment. Will prices turn north again before the Fed starts this new policy?

Labels: economics, Federal Reserve, money

Thursday, February 11, 2010

Bye-bye Fed funds target

The text is here. In it Bernanke also suggests a new instrument for removing excess reserves from the system, a term deposit banks could make to the Fed that would compete with Treasuries as a store of liquidity for them.�Although at present the U.S. economy continues to require the support of highly accommodative monetary policies, at some point the Federal Reserve will need to tighten financial conditions by raising short-term interest rates and reducing the quantity of bank reserves outstanding,� he wrote.

�We have spent considerable effort in developing the tools we will need to remove policy accommodation, and we are fully confident that at the appropriate time we will be able to do so effectively.�

Mr. Bernanke, however, did provide new details of a major concern: how, as the recovery proceeds, to gradually shrink the balance sheet, which along with a vast array of assets also includes $1.1 trillion that banks are holding with the Fed.

Mr. Bernanke suggested that a new policy tool � the interest rate on excess reserves, which the Fed began paying in October 2008 � would be a vital part of the Fed�s strategy.

Increasing that interest rate, he said, will have the effect of pushing up other short-term interest rates, including the benchmark fed funds rate � the rate at which banks lend to each other overnight.

The Federal Reserve would likely auction large blocks of such deposits, thus converting a portion of depository institutions' reserve balances into deposits that could not be used to meet their very short-term liquidity needs and could not be counted as reserves. A proposal describing a term deposit facility was recently published in the Federal Register, and we are currently analyzing the public comments that have been received. ... we expect to be able to conduct test transactions this spring and to have the facility available if necessary shortly thereafter. Reverse repos and the deposit facility would together allow the Federal Reserve to drain hundreds of billions of dollars of reserves from the banking system quite quickly, should it choose to do so.Both new instruments provide a means by which the Fed can increase its balance sheet without impacting the money supply, by inducing banks not to use their excess reserves for deposit expansion. I was familiar with both these instruments in Macedonia, where excess reserves were close to 30% of the money supply. The problem there was that it created flabby banks unwilling to lend, since easy government revenue was close at hand. The Fed does not directly spend taxpayer dollars, but its remission of excess earnings from its portfolio to the Treasury would be shifted to banks, and that indirectly expands the government's need for additional debt to cover its spending. That's not likely to go over well.

The biggest signal was not a date but a statement that the Federal funds rate would no longer be a policy instrument for the Fed, at least for awhile:

As a result of the very large volume of reserves in the banking system, the level of activity and liquidity in the federal funds market has declined considerably, raising the possibility that the federal funds rate could for a time become a less reliable indicator than usual of conditions in short-term money markets. Accordingly, the Federal Reserve is considering the utility, during the transition to a more normal policy configuration, of communicating the stance of policy in terms of another operating target, such as an alternative short-term interest rate. In particular, it is possible that the Federal Reserve could for a time use the interest rate paid on reserves, in combination with targets for reserve quantities, as a guide to its policy stance, while simultaneously monitoring a range of market rates. No decision has been made on this issue; we will be guided in part by the evolution of the federal funds market as policy accommodation is withdrawn. The Federal Reserve anticipates that it will eventually return to an operating framework with much lower reserve balances than at present and with the federal funds rate as the operating target for policy.The last time the Fed abandoned the Fed funds target was October 1979, when then-Chair Paul Volcker thought it more prudent to stop inflation by using a target on reserves. That lasted perhaps three years, maybe less (see Alton Gilbert for more.) That period led to rather high volatility in interest rates may have contributed to the double-dip recessions in 1980-82.

It would be fair criticism of the above to say we really haven't used the Fed funds target for awhile and that this is just recognition of reality. But the FOMC statement still focused on it, and the Fed had not enunciated until yesterday what we might look at for an alternative target. Now we have. This will make reading the next FOMC statement on March 16 very interesting indeed.

UPDATE: John Taylor doesn't like the term deposits from the Fed to the banks.

In my view, Fed borrowing instruments should be avoided as much as possible because they delay essential adjustments in reserves and create precedents which make it easier to deviate from the monetary framework in the future. Similarly, the instrument of paying interest on reserves to achieve the short term interest rate target should be used only during a well defined transition period.He argues instead for a rule that ties Fed fund rate increases to a decrease in reserves. It would make Fed policy more predictable.

[P]olicy makers could treat this exit rule as an exit guideline rather than a mechanical formula to be followed literally, much as a policy rule for the interest rate is treated as a guideline rather than mechanical formula. They would vote on how much to reduce reserves at each meeting along with the interest rate vote. Note that the exit rule would we working in tandem with a policy rule for the interest rate, such as the Taylor rule.With all that's going on in Europe, this might be sliding under the radar. It shouldn't.

Labels: economics, Federal Reserve, money

Friday, January 22, 2010

Bernanke a victim of Brown-mania?

Hard to believe, but the Bernanke reconfirmation may be in serious trouble. Ed Morrissey fleshes out the story. The stock market sags partly in response. The WSJ Market Beat blog has a roundup of economists' reactions. A current tally shows 17 votes for reconfirmation, 12 against (including five Democrats), with five more Democrats answering that they are at this time undecided. Many of the Democrat opponents, including Barbara Boxer and Russ Feingold, announced their opposition today. Majority Leader Reid and Minority Leader McConnell are now jointly counting noses to see if they have 60 votes (as the more anti-Fed types like Jim Bunning are placing a hold on Bernanke's nomination.)

Opposition to the Fed chair seems to have increased since the election of Scott Brown on Tuesday. The Huffington Post reports this afternoon that

We get this rather unprincipled announcement from Sen. Boxer:The election in Massachusetts has senators who previously considered themselves safe watching their backs, and they don't relish the prospect of a vote in favor of a man who failed to foresee the financial crisis and is closely associated with Wall Street.

A recent poll found that 47 percent of Americans think Bernanke cares more about Wall Street than Main Street, while only 20 percent think he works for Main Street. Independents, who swung heavily for Brown in Massachusetts, are even more opposed to Bernanke than Democrats or Republicans. Fifty percent of independents think he cares first about Wall Street; 15 percent think he prioritizes the needs of Main Street. That's a difficult vote in the face of an angry public.

If Bernanke is confirmed, he'll have to rely on the same coalition that moved the bailout through Congress, when the leadership of both parties joined forces to oppose the rank and file.

No, Senator, it is not the job of the Federal Reserve to be a champion for Main Street, Wall Street, or anyone else. The Federal Reserve is an independent institution, a feature that Congress chose wisely almost a century ago."I have a lot of respect for Federal Reserve Chairman Ben Bernanke. When the financial crisis hit in late 2008, he took some important steps to prevent what many economists believe could have been an even greater economic catastrophe," said Boxer.

"However, it is time for a change -- it is time for Main Street to have a champion at the Fed. Dr. Bernanke played a lead role in crafting the Bush administration's economic policies, which led to the current economic crisis. Our next Federal Reserve Chairman must represent a clean break from the failed policies of the past."

The Fed, as Robert Samuelson points out, has had officials testify before Congress 32 times. Its actions are not a secret, and attempts to find out who got direct loans from the Fed are more meant to intimidate than illuminate. The assault on its independence has helped push down stock prices and could set off a currency crisis in a G-7 currency, which is extraordinary. At a time where financial crisis still looms large in the rear view mirror, it is highly irresponsible to engage in scapegoating.First, central bank independence has been shown to be essential for controlling inflation. Sooner or later, the Fed will have to scale back its current unprecedented monetary accommodation. When the Federal Reserve judges it time to begin tightening monetary conditions, it must be allowed to do so without interference. Second, lender of last resort decisions should not be politicized.

Finally, calls to alter the structure or personnel selection of the Federal Reserve System easily could backfire by raising inflation expectations and borrowing costs and dimming prospects for recovery. The democratic legitimacy of the Federal Reserve System is well established by its legal mandate and by the existing appointments process. Frequent communication with the public and testimony before Congress ensure Fed accountability.

Overnight, every senator realized the quickest, easiest way to populist street cred is to treat Bernanke like he's the third Salahi.

Labels: banking, economics, Federal Reserve, money

Thursday, December 24, 2009

Not too fast

Business loans on the balance sheets of all federally insured U.S. banks fell $89.1 billion, or 6.5%, from July 1 to Sept. 30, according to the Federal Deposit Insurance Corp. That was part of a $210-billion drop in overall loans outstanding, the largest such decline since at least 1984.

"In some ways, the pendulum may have swung too far in the direction of not lending, after a decade in which it had gone way too far in the direction of getting money out the door, no matter the risk," Obama said. "If we can get that balance right . . . there are businesses and communities out there that are ready to grow again."

Prof. Charles Goodhart is seeing a similar story in Britain.

Prof. Charles Goodhart is seeing a similar story in Britain."What has happened to all the monetarists? Growth in money holdings and lending has plummeted. Thirty, or 40, years ago they would have been forewarning doom and destruction at this juncture, and casting anathemas at the authorities," he wrote in a consultant report for Morgan Stanley.

"There is a danger that markets and authorities become obsessed about the fiscal implications of the crisis at a time when the real worries should still focus on private sector access to credit and money."

Did anyone ask Bernanke about this in confirmation hearings earlier in the month? No, and the closest answer we got in written responses was that to Brad DeLong's 3% inflation target question, which Scott Sumner excoriated.

The risk is that we don't know where the Fed is heading next between this and the . Nariman Behravesh of Global Insight is nervous:

Would tightening credit in Q1 or Q2 be an example of "botched" monetary policy? (Thanks to Gary for the last link.)"Any number of risk could knock us back down into recession," ... These risks include botched monetary policy by the Fed, a major retrenchment of consumer spending in the face of rising unemployment, and another chapter to the financial crisis.

Behravesh isn't saying it's the most likely scenario; but at 20% the probability is "too high" for his liking.

Labels: economics, Federal Reserve

Wednesday, December 09, 2009

A little too much PR?

I had wondered about this last night and spent a few minutes today re-reading Donald Kettl's Leadership at the Fed. While the Fed maintains a political independence, he argues, it's up to each chairman or chairwoman to build support to keep it.

Throughout the Fed's history, its power over the economy has depended more on the political leadership of its chairman than on any other factor. Both the friends and enemies of the Fed focus on its unrivaled legal independence, but that independence is only a precondition for power, not power itself. The Fed's power depends on the support it can build, not on its legal status. Without political support, its credibility is low, its effectiveness is sharply limited, and its legal independence is fragile. Indeed, as the Fed's history shows, its much-vaunted legal independence is most important because it provides the flexibility for building support. And this central job -- of building support, of developing credibility, of dealing with the complex and conflicting political environment in which the Fed finds itself -- has been the central job of the chairman. (193)Chairman Bernanke, when he was an academic and when he was a governor of the Fed, was a strong advocate of increasing transparency, including his support of inflation targeting (see Bernanke and Mishkin [1997] and Bernanke [2003], e.g.) But he's had to learn that transparency doesn't always mean that one's actions are understood. And transparency doesn't always mean you build support for your actions. Harry Reid is perhaps too transparent on health care these days, for example. If I was a Democratic adviser, I'd tell the man to button his lip.

Has Bernanke built support by his statements? Judging by his poll numbers you'd have to say no. (Support was about 50-50 in October 2008 when the Lehman/Merrill/AIG hit the fan.) A Gallup poll of Greenspan in 2005 found only 20% of Americans had a "great deal" of faith in his ability to manage the economy -- and that's when the economy was not in recession. It was at 29% in April 2001. Barry Ritholz has a Bernanke approval graph. It is worth noting, as Kettl does, that after the wrenching recession of 1981-82, 46% of Americans felt Paul Volcker had made "a major contribution" to lower inflation and 64% were willing to have the Fed tighten money again if inflation reappeared. If we had another banking panic, would Bernanke have that kind of support?

Support means, though, support from the Congress and the executive branch. The Senate Banking Committee votes on his re-confirmation next week and it looks like he'll pass, though with several dissents. The same most likely when the full Senate votes, probably in January. The magic number on the Senate floor will be 19, though. That's the number of senators who didn't vote for Volcker's reappointment in 1983. No Fed chair has ever had 20 noes.

Labels: economics, Federal Reserve

Monday, December 07, 2009

Mattress stuffers

Demand for �50 notes has risen sharply during the recession because the public has lost faith in the banks, the Bank of England's chief cashier Andrew Bailey has suggested.Source. That got me to wonder how much we are issuing in $100 bills here in the USA. Turns out the data is only annual, but we did issue $55 billion additional C-notes in 2008. As of November 23, there isn't much more in total currency issued -- no breakdown of the size of the notes there. Then again, when your economy contracts you would expect lower demand for currency, which makes the UK figures all the more surprising.

..."Two features of the current situation strike me as most relevant in explaining this development: first, lower levels of public confidence in the banking system and second, low interest rates," he said.

UPDATE: Paul Murphy suggests a third reason: worker remittances. But if anything remittances are down, not up in 2009. I have had several reports on lower remittances into Armenia this year, perhaps by more than a third from 2008.

Labels: economics, Federal Reserve, money

Wednesday, November 04, 2009

Where does interest on reserves come from?

[Y]esterday I was trying to teach the consequences of paying interest on reserves to my bright high school students. They got, correctly, that paying interest on reserves lowers the money multiplier (it makes banks want to hold more reserves, which lowers the amount of lending they do for a given supply of reserves from the Fed) and is therefore contractionary.

But one student asked, "Doesn't paying interest on reserves increase the deficit, and isn't that expansionary?" My response was to say that this is correct...

But the Federal Reserve does not draw money from the Treasury to pay interest. It pays it out of its own earnings on its portfolio. Look at its (audited!) financial statements here, and see page 5. You'll see a line item for "depository institution deposits" under "interest expenses." The Fed remits the excess of its income less expenses to the Treasury (see the line "payments to U.S. Treasury as interest on Federal Reserve notes") which was in 2008 lower. But net interest income didn't change, so you would be hard pressed to say that paying interest increased the U.S. federal deficit.

Likewise would have been my response to increasing reserve requirements. However, I agree with Kling that the signal that would have created would have been potentially more damaging than paying interest on excess reserves. Doing the latter does, I think, increase the marginal cost of lending to the bank, and thus reduce loans. (Paying interest on required reserves, on the other hand, is just a pure transfer of income from the Fed to commercial banks.)

My thanks to my colleague Eric Hampton for thinking this through with me.

Labels: economics, Federal Reserve

Tuesday, October 27, 2009

Can FDIC solve "too big to fail" for non-banks?

I agree with this -- in fact, did last month -- but it has been clear for awhile that the Fed didn't want this role. In fact, the college of regulators is a Bernanke idea from a few weeks ago. You might argue Bernanke was just seeing the handwriting on the wall, but I doubt many in the Fed disagree with Vincent Reinhart's appraisal.Under this authority, jokingly referred to as "Death Panels for Banks," the Federal Deposit Insurance Corp. would oversee the dismantling of large financial firms much as it does now when it intervenes in commercial banks that are at risk of insolvency.

Decisions about which institutions are so large that they pose a system-wide risk and must be monitored would be made by a Council of Regulators, comprised of leaders from the Fed, the Treasury Department, the FDIC, and other bank-oversight agencies.

...Some independent analysts also have warned that handing the Fed new, expansive powers as the systemic risk regulator could distract it from its principal role of setting monetary policy to sustain growth and contain inflation."I didn't want the Fed to have that role because I think monetary policy is too important," said Vincent Reinhart, a former top Fed economist who's also wary of the emerging legislation. "If all you do is a college of regulators, that's just inviting a debating society."

Reinhart and Fed governor Dan Tarullo have both argued in the last week that the problem is too-big-to-fail and that the issue is how to deal with non-bank financial giants like Lehman and AIG, for which regulators had to improvise. (See the McKinley and Gegenheimer timeline FMI.) If these companies are going to be placed under some government protection in a too-big-to-fail environment, I have to disagree with Ed that they don't get some kind of regulation. You may own a skyscraper as your private property, but when you tear it down you're responsible for any damage done to nearby buildings. If a private non-bank fails and in the process takes down healthy financial institutions that were counterparties, you may have a reason for using the law to limit collateral damage. (That doesn't mean you always get it right, as John Carney points out in the AIG case.)

So what can be done, if we're not going to use the Fed or FDIC? Before you say "we have to do something", consider the benefits of large banks, says Charles Calomiris. Diversification, economies of scope and extended reach to developing markets are some of these benefits. Are we at risk of losing those gains as we try to solve too big to fail?

UPDATE: John Taylor summarizes the testimony around Frank's FDIC proposal.

Labels: banking, economics, Federal Reserve

Friday, September 18, 2009

A dangerous expansion

I know some readers will take up the "where in the Constitution does it say" charge. It's a legitimate point, but not likely to be very effective as an argument. And there is the reasonable point that the Federal Reserve does not do compensation studies and has no specific knowledge that makes it more able to do this than, say, the Department of Labor.Under the proposal, the Fed could reject any compensation policies it believes encourage bank employees -- from chief executives, to traders, to loan officers -- to take too much risk. Bureaucrats wouldn't set the pay of individuals, but would review and, if necessary, amend each bank's salary and bonus policies to make sure they don't create harmful incentives.

A final proposal is still a few weeks from completion and could be revised along the way, according to people familiar with the matter. It requires a vote by the central bank's board, but no congressional approval.

The U.S.'s largest banks, about 25 in number, would get especially close scrutiny. The central bank intends to compare these banks as a group to see if any practices stand out as unusually dangerous to their firms.

Let me set those points aside.

The Federal Reserve is supposed to have independent status. As Dallas Fed president Richard Fisher pointed out a couple of years ago, at times the Fed has been less independent and at other times more so. Less in the 1960s, more in the 1980s and 1990s. Which Fed gave this country better performance? Not versus an ideal, mind you, just better. I don't think you would find many economists who thought the William McChesney Martin Fed performed better than the Paul Volcker Fed. For all the mistakes Greenspan made, his performance was better than Arthur Burns'.

Why? Is its independence part of the reason? Fisher writes:

Under Chairmen Alan Greenspan and Ben Bernanke, the Federal Reserve has been left alone to conduct monetary policy. We are a truly independent central bank. Policy is set by the Federal Open Market Committee. The 17 current participants in the FOMC deliberations consist of five governors, including the chairman, who are appointed by the president of the United States and confirmed by the Senate, and 12 presidents of the Fed�s regional Banks, each of whom serves at the pleasure of his or her Bank�s board of directors. All 17 participate in honest and vigorous discussion of the economy and each offers his or her individual policy prescription at FOMC meetings convened and presided over by the chairman. At the end of these meetings, the chairman calls for a vote.And where does that independence come from? Not the Constitution; monetary policy is the purview of the Congress, and the Fed is an agency delegated powers by the Congress. The question is what powers can you delegate to the Fed and still call it independent?

I think executive pay compensation is a particularly dangerous delegation to the Fed's ability to conduct monetary policy. Money is created not only by the Fed but by bank lending; if a central bank can control pay, it can influence bank lending. This makes the Fed less transparent when most everyone seems to agree that more transparency is needed.

I have the same fears regarding the Fed as a super-regulator. I would point out this wise advice from the Indian economist Ajay Shah last week:

[I]ndependence goes with a narrowing of the functions of the central bank. There is no economic case for having independence from politicians for functions such as running the payments system, regulating or supervising financial markets or banks, running a bond exchange and depository, manning a system of capital controls, etc. The rationale for independence is limited to one specific problem: that of setting the short-term interest rate of the economy. Hence, giving RBI [Reserve Bank of India --kb] independence requires narrowing down its functions to the core where economic logic suggests independence. All other functions need to be placed in conventional agencies, with control in the hands of accountable politicians.There's some places to quibble there -- why short-term interest rates, for example, and not the exchange rate or the stock of money? -- but in general Shah makes an excellent point. You might want another agency that regulates financial firms to be independent of political control. But the best central banks seem to be those that, to use Willem Buiter's words, stick to their knitting and avoid commenting on everything other than interest rate or exchange rate policy.

This proposed U.S. policy goes in exactly the opposite direction. It is a danger to our monetary system, and should be opposed immediately.

Labels: economics, Federal Reserve

Monday, September 14, 2009

Fixing what you can't see

The Wall Street Journal, at least, has taken notice.

Vern's documents are all published at Scribd. The feds, of course, would like to get a judge to simply throw out these cases, but Judicial Watch is currently on this case.Last December, Mr. McKinley sent a FOIA request to the Fed to find out what Fed governors meant when they said a Bear Stearns failure would cause a "contagion." This term was used in the publicly-released minutes of the Fed meeting at which the central bank discussed plans by the Federal Reserve Bank of New York to finance Bear's sale to J.P. Morgan Chase. The minutes contained only the vague warning of doom, without any detail on how exactly the fall of Bear would destroy America. Mr. McKinley's request sought the supporting documents for this conclusion.

He also requested minutes of the autumn FDIC board meeting at which regulators approved financing for a Citigroup takeover of Wachovia. To provide this assistance, the board had to invoke the "systemic risk" exception in the Federal Deposit Insurance Act, and therefore had to assert that such assistance was necessary for the health of the financial system. Yet days later, Wachovia cut a better deal to sell itself to Wells Fargo, instead of Citi. So how necessary was the FDIC's offer of assistance?

After Mr. McKinley sued the agency this summer, the FDIC coughed up a previously undisclosed staff memo to the FDIC board. Again, the agency redacted the substance, providing roughly two pages of text from the nine-page original. The section of the memo titled "Systemic Risk" was entirely erased. As for the Fed, it blew off Mr. McKinely's initial request and has since responded mainly with some highly uninformative letters from the Fed staff to Congress.

Many of FDIC's actions are relatively routine. Its closure over this weekend of $7 billion Corus Bank of Chicago, however, contains a "private placement" of $4 billion of Corus assets. How private is this? Who is the purchaser, and how many bids are there? One would think this is public information. Researchers like Vern are simply interested in writing the history of this unique moment in international finance.

The WSJ concludes:

A public debate on which banks really needed a bailout via the government's AIG conduit has hardly taken place. And did all of Bear Stearns' creditors, including hedge funds, need to be made whole to ensure the survival of American capitalism?A year after the epic meltdown, this is the debate Congress needs to undertake before legislating any new federal authority. Regulators should not receive a blank check to prevent systemic risk without even defining what that term means.

Labels: banking, Federal Reserve

Tuesday, September 01, 2009

Reference cycles

Why is this important? In the 1973-75 case the answers given by the government (Nixon/Ford) and the Fed (Arthur Burns) were a combination of "we're all Keynesians now" and the disastrous wage and price controls and incomes policies (culminating in Whip Inflation Now buttons.) The 1981-82 period was the Volcker disinflation, Reagan tax cuts, etc.The facts we face today are very different than the grim reality Americans confronted between 1929 and 1932. True, this recession is not over. But it would have to get improbably worse before it came close to the 42-month duration of the Great Depression, or the 25% unemployment rate in 1932. Then, the only safety net was the soup line.

The current recession is also much less severe than the 1937-38 Depression. A more accurate comparison is to the 1973-75 recession. Today's recession is as deep and most likely won't be much longer than the one we experienced some three decades ago. By pointing this out, I do not intend to minimize the damage that the economic crisis has had on individuals and businesses. But as policy makers make decisions in order to alleviate the recession, they are not helped when economists overstate its severity.

The table nearby compares the current recession, the 1937-38 depression and some past severe postwar recessions. If the recession ends this summer�as many experts predict�the record will show that it was not very different from other postwar recessions, but very different from the 1937-38 and 1929-32 Depressions.

Which worked out well? Which worked out poorly? And which does current policy remind you of more? Maybe more than students of the Great Depression, we need policymakers who are students of the 1970s.

Labels: economics, Federal Reserve

Friday, August 28, 2009

Stopped clock or red flag?

Meet your newest friend: Barney Frank.

Secondly, they have has since 1932 a right under Herbert Hoover to intervene in the economy whenever they could. Last September, the Federal Reserve they were going to advance $82 billion to AIG. I was kind of surprised and said, 'Mr Bernanke do you have $82 billion?' Mr. Bernanke replied, 'I have $800 billion and under section 13.3 of the Federal Reserve Act they can lend anything they want.'So is Barney Frank one of you Jekyll Island theorists? Is he just a stopped clock that's right twice a day? Or do you realize that you may be helping to hand the keys to monetary policy over to Nancy Pelosi?

We are going to curtail that lending power. We are going to put some restrictions on it.

Finally we will subject them to a complete audit. I have been working with Ron Paul, who is the main sponsor of that bill. He agrees that we don't want to have the audit appear as if influences monetary policy as that would be inflationary.

One of the things the audit will show you is what the Federal Reserve buys itself. And that will be made public, but not instantly because if it was made instantly people would be trading off it, so the data would be released after a time period of several months, enough time so it will not be market sensitive. This will probably pass in October.

Everyone who believes the audit run by Pelosi and Frank will not "influence monetary policy" in a way that would be inflationary, raise your hand. How about you, Rep. Bachmann?

Labels: economics, Federal Reserve

Tuesday, August 25, 2009

Quick note on Bernanke's reappointment

The better question is really why now? Why reappoint Bernanke five months ahead of schedule, while President Obama is supposed to be vacationing? My only answer is that the Administration wants his position secure as they prepare to restructure financial regulation. I think it makes it more rather than less likely that the Fed is getting the keys to a new souped-up regulatory machine. More on whether I like that or not when we get closer to having a proposal from Congress.

Labels: economics, Federal Reserve

Fewer secrets of the temple

Vern should therefore be encouraged by last night's ruling that the news agency Bloomberg will be given access to a list showing who received emergency loans from the Fed. The documents requested were to determine not only who got loans under the Fed's Primary Dealer Credit Facility but what kinds of collateral were pledged against the loans. The same was requested for three other facilities: the traditional Fed discount window, the Term Auction Facility and the Term Security Lending Facility. Just as in Vern's case, the Federal Reserve said FOIA has exceptions that permit them to deny Bloomberg's request. Separately, Bloomberg sought data on the Bear Stearns bailout, and the collateral pledged in that request to the Fed. Again, nothing. The court has ruled that the exceptions to FOIA that the Fed wished to use are not applicable to the information Bloomberg sought.

Vern rights that this ruling is "good news" for his case. Investigation of what happened in 2008 is vital; one hopes that the information will be useful in the upcoming reappointment hearings for Fed Chair Bernanke.

Labels: economics, Federal Reserve, money

Friday, August 21, 2009

Benanke: a U, not a V, and a me

Overall, the policy actions implemented in recent months have helped stabilize a number of key financial markets, both in the United States and abroad. Short-term funding markets are functioning more normally, corporate bond issuance has been strong, and activity in some previously moribund securitization markets has picked up. Stock prices have partially recovered, and U.S. mortgage rates have declined markedly since last fall. Critically, fears of financial collapse have receded substantially. After contracting sharply over the past year, economic activity appears to be leveling out, both in the United States and abroad, and the prospects for a return to growth in the near term appear good. Notwithstanding this noteworthy progress, critical challenges remain: Strains persist in many financial markets across the globe, financial institutions face significant additional losses, and many businesses and households continue to experience considerable difficulty gaining access to credit. Because of these and other factors, the economic recovery is likely to be relatively slow at first, with unemployment declining only gradually from high levels.Up to the last two sentences it sounded like he was popping a cork. Arnold Kling is even more critical than I am. The role of Bernanke in the decisions on Bear, Lehman, and Merrill Lynch are not uniform, but Kling notes that Bernanke portrays the latter two as part of a grand strategy.

There [sic] word "panic" appears 14 times during the speech. The phrase "house prices" appears just twice, and the phrase "mortgage defaults" appears just once.But the market seemed to like it, with the Dow shooting up 1.5% in the first 90 minutes of trading. So the question to market participants is, what did you learn from this that you didn't know before? Is the U-shaped recovery a signal that the Fed will keep interest rates down long? What does that mean for inflation (gold is up $13 as I type this)? Why would Bernanke not reflect on the housing market where foreclosures continue to climb?Clearly, Bernanke was listening to the CEO's of the big financial institutions who were telling him that they would have been fine if their short-term lenders had stuck by them. As far as the big bankers were concerned, this was an immaculate panic, in which their actual bad investments were not the problem. It was just that too many people lost confidence.

If this story is true, then whoever invested in banks and "toxic assets" last year should end up with a huge profit. The taxpayers should be raking in tens of billions, if not hundreds of billions, in windfall gains over the next few years, as the Fed and the Treasury cash in on the investments they made while everyone else was in panic.

And before you pop a cork even on banks (what with the government deciding it doesn't need the last $250 billion of TARP), what about the 77 FDIC-closed institutions so far this year? Floyd Norris writes:

Although the losses on current failures stem mostly from construction loans, it is possible that commercial real estate will be the next big problem area. Losses in that area were growing at the Temecula bank, although its portfolio was relatively small.I was on KNSI this morning, extending into Hot Talk when the Ox called in sick. Co-host Mike Landy asked me whether we have the right team in place to run whatever exit strategy we have. "We have smart people in the top places," I answered, "but these same people were there three years ago." I would like to see more learning and less cheering.

During the credit boom, loans on those properties became easier and easier to get, on more and more liberal terms. Unlike residential mortgages, commercial real estate loans typically must be refinanced every few years. With rents and values down in many areas, that will not be possible for a lot of buildings, and some owners are just walking away from their buildings.

Two years ago, when the subprime mortgage problems began to surface, Washington took great comfort from solid balance sheets, which regulators thought meant the banks could easily weather the problem.

Last year, we learned that the regulators, like the bankers, did not comprehend the risks of some of the exotic instruments dreamed up by financial engineers. This year we are learning that the regulators, like the bankers, also failed to understand the risks of the generous loans that the banks were making in the middle of this decade.

Labels: economics, Federal Reserve, money

Wednesday, August 12, 2009

Don't get too excited

Information received since the Federal Open Market Committee met in June suggests that economic activity is leveling out. Conditions in financial markets have improved further in recent weeks. Household spending has continued to show signs of stabilizing but remains constrained by ongoing job losses, sluggish income growth, lower housing wealth, and tight credit. Businesses are still cutting back on fixed investment and staffing but are making progress in bringing inventory stocks into better alignment with sales. Although economic activity is likely to remain weak for a time, the Committee continues to anticipate that policy actions to stabilize financial markets and institutions, fiscal and monetary stimulus, and market forces will contribute to a gradual resumption of sustainable economic growth in a context of price stability.It's that last line that will create a buzz more than the "leveling out", as it's an indication that the period of quantitative easing may have reached its apex. But let's remember all the steps they've taken. The New York Times points to the $1.25 trillion purchase of mortgage-backed securities as evidence this hasn't come to an end yet. It still is running $100 billion auctions on a regular basis.

...The Committee will maintain the target range for the federal funds rate at 0 to 1/4 percent and continues to anticipate that economic conditions are likely to warrant exceptionally low levels of the federal funds rate for an extended period. As previously announced, to provide support to mortgage lending and housing markets and to improve overall conditions in private credit markets, the Federal Reserve will purchase a total of up to $1.25 trillion of agency mortgage-backed securities and up to $200 billion of agency debt by the end of the year. In addition, the Federal Reserve is in the process of buying $300 billion of Treasury securities. To promote a smooth transition in markets as these purchases of Treasury securities are completed, the Committee has decided to gradually slow the pace of these transactions and anticipates that the full amount will be purchased by the end of October.

Labels: economics, Federal Reserve, forecasting

Thursday, August 06, 2009

Lay down with dogs...

Wall Street banks and lawyers could collect nearly $1 billion in fees from the Federal Reserve Bank of New York and American International Group Inc to help manage and break apart the insurer, The Wall Street Journal said on Wednesday, citing its own analysis.You'll no doubt note the numerous TARP recipients on that list. But if the government owns 80% of a company and wants to break it up, it probably doesn't have its own mergers and acquisitions department. Nor should it. Still, it's one of those little surprises that will continue to haunt the government that decided to support AIG rather than let it fail.Morgan Stanley could collect as much as $250 million, the newspaper said, citing banking experts and documents released by the New York Fed.

Bank of America Corp, private equity firm Blackstone Group LP, law firm Davis Polk & Wardwell LLP, accounting firm Ernst & Young, Goldman Sachs Group Inc and JPMorgan Chase & Co are among others that have or could get big paydays for helping dismantle AIG, the newspaper said.

To put it in context, market capitalization for the company is $3.18 billion. The government owns 80% of that, or $2.54 billion.

Labels: economics, Federal Reserve, money

Monday, August 03, 2009

The Fed Audit bill is about Congress taking over monetary policy

It is important to remember that the GAO already has the authority to audit the Fed, and does, except that the bill giving the GAO this authority in 1978 specifically excluded certain aspects of the Fed�s activities from GAO audits � essentially, decisions about monetary policy. The only purpose of the new bill is therefore to decrease the Fed�s independence with regard to monetary policy decisions.To verify that, I dug up a Congressional Research Service report from 2005:

The Federal Banking Agency Audit Act (P.L. 95-320) was enacted in 1978 to enhance congressional oversight responsibilities. The law gave the General Accounting Office (GAO; now the Government Accountability Office) the authority to audit the Board of Governors, the Reserve Banks and branches. Such audits are limited, however, as GAO is prohibited from auditing monetary policy operations, foreign transactions, and the FOMC operations. Congressional oversight on these matters is exercised through the requirement for reports and through semi-annual monetary policy hearings.Here's the Fed's 2008 audits, and the last page shows the audits done by GAO.

Do you think the Congress should have the GAO audit monetary policy, rather than having this done in Humphrey-Hawkins testimony? Some conservatives do. Professor Woodford points out the dangers:

The dangers are especially great at a moment like the present one, when the prospect of large government deficits for years to come could easily make short-sighted decisions to use monetary policy to facilitate the financing of those deficits all too tempting. It is ironic that many of the proponents of reining in the Fed claim that their concern is preventing the Fed from further weakening the value of the currency, when the opposite would almost certainly be the consequence of their bill if passed.

Labels: economics, Federal Reserve, money

Monday, July 20, 2009

What would you replace the Fed with?

But Henderson appears to have had a change of heart, calling the Fed "illegitimate," even while maintaining it is more transparent than most government agencies. Meanwhile, Arnold Kling and Alex Tabarrok argue that the Federal Reserve suffers from a kind of regulatory capture by commercial banks. Here's Kling:

I perceive signs of what Danny Kaufmann calls "cognitive capture" of the Fed by the banks that it regulates. That is, the Fed sees the world through the eyes of the executives at large banks.And Tabarrok, at greater length:

But neither point out that the Federal Reserve is in fact owned by commercial banks, specifically for that reason. The problem with a dependent central bank is a time-consistency problem. (Not long ago we thought enough of it to award a Nobel to its discoverers.) Central banks can promise price stability but, when they are subject to an electoral check, they can't deliver on the promise because of the possibility of temporarily raising output in advance of an election and having inflation come later (the "political business cycle", a topic I first wrote about in graduate school.) Central banks cannot make credible commitments to price stability without overcoming the problem.The primary reason that independent central banks are better at controlling inflation is that absent direct political control the default selection mechanism favors bankers, i.e. lenders, people whose interests make them more favorable towards lower inflation.

Thus, independence is a political decision that favors lenders in the decisions of monetary policy. Now, depending on the alternatives, there may be good reasons for making this choice but we should not fool ourselves into thinking that we have depoliticized money. We should not be surprised, for example, that "independent" central banks tend to make lender of last resort decisions that protect banks and bankers.

It's true that a central bank could find another mechanism to overcome the problem, such as the Reserve Bank of New Zealand's contract that fires a central bank governor if he allows inflation to rise above a certain rate. Tabarrok notes this example as a case where the central bank does NOT have independence. But independence means two different things: It can mean independence of choosing its goals, or it could mean independence in choosing the instruments by which it meets those goals. You can tell me to keep inflation below 2% or I'm fired, but you permit me to use whatever means I wish to meet that target. Tabarrok misfires in calling the New Zealand central bank dependent. See Carlstrom and Fuerst [2006].

In the absence of a contract, one can choose instead to delegate monetary policy to someone who can overcome the time inconsistency problem. The old story we use in classrooms is to think about a father taking his two sons to a baseball game; the family goes once a year; the stadium is a three-hour drive from home. Brothers often fight in back seats, so the father turns around and tells them "stop or we won't go to the game." Of course the sons don't believe Dad, because Dad loves baseball, they know he does, and turning the car around is too painful for Dad. Delegation means giving the tickets to Mom, who let's say doesn't like baseball. "If you don't behave, Mom will not give us the tickets to go to the game." (I can't take credit for this metaphor -- it was in an intermediate macro text I read and used, but I can't find where I got it on my bookshelf. Apologies to the originator of that story.)

A government official cannot make a credible commitment to price stability, because if some price shock happens the cost of keeping the commitment is high unemployment which is painful to the government official. So he delegates monetary policy to someone who cares less about unemployment than he does, and cares perhaps more about price stability. That is in fact exactly what a commercial banker prefers.

Federal Reserve governors are chosen by the president subject to confirmation by the Senate. But Federal Reserve bank presidents (of the twelve branches) are chosen by the members of the Fed, the commercial banks. They are typically more inflation averse than the governors (see Havrilesky and Gildea [2007], for example.) In some cases the central bank's board is entirely chosen by bankers (see Swiss National Bank for example.)

The reasons for central bank independence at this particular time in history are, I believe, profound. James Hamilton writes:

The reason I find that loss of Fed independence to be a source of alarm is the observation that every hyperinflation in history has had two ingredients. The first is a fiscal debt for which there was no politically feasible ability to pay with tax increases or spending cuts. The second is a central bank that was drawn into the task of creating money as the only way to meet the obligations that the fiscal authority could not. Every historical hyperinflation has ended when the fiscal problems got resolved and independence of the central bank was restored.I return to the question I asked before: if you abolish the Fed, what do you replace it with? Tabarrok's complaint that even delegating to commercial bankers makes it political would seem to lead to a complaint about governments maintaining a monopoly over money. Would only competitive money satisfy the objections? I suspect it would prevent hyperinflation, but multiple monies are also likely to sacrifice many scale economies that allow our current level of financial sophistication.

Labels: economics, Federal Reserve, inflation

Wednesday, July 15, 2009

Petition on central bank independence

Link added in cite. Some of my writings on the subject are here, here, and here.Amidst the debate over systemic regulation, the independence of U.S. monetary policy is at risk. We urge Congress and the Executive Branch to reaffirm their support for and defend the independence of the Federal Reserve System as a foundation of U.S. economic stability. There are three specific risks that must be contained.

First, central bank independence has been shown to be essential for controlling inflation. Sooner or later, the Fed will have to scale back its current unprecedented monetary accommodation. When the Federal Reserve judges it time to begin tightening monetary conditions, it must be allowed to do so without interference. Second, lender of last resort decisions should not be politicized.

Finally, calls to alter the structure or personnel selection of the Federal Reserve System easily could backfire by raising inflation expectations and borrowing costs and dimming prospects for recovery. The democratic legitimacy of the Federal Reserve System is well established by its legal mandate and by the existing appointments process. Frequent communication with the public and testimony before Congress ensure Fed accountability.

If the Federal Reserve is given new responsibilities every effort must be made to avoid compromising its ability to manage monetary policy as it sees fit.

Labels: economics, Federal Reserve, politics

Monday, July 13, 2009

What he said

What we want is an independent Federal Reserve that won't be kow-towed by politics. The fact is that there's no way a new, Congressionally audited Federal Reserve could ever be more independent of Congress. That's just impossible. Even if some Congressmen have principled objections to the way the institution has handled itself during the crisis, that's doesn't describe the motivations of the whole body, which just wants to expand its power.Source. See prior posts here and here.If you want a Fed that will stand up to Congress -- not print money every time Congressmen want to spend it -- then the last thing that makes sense is to make the Fed more answerable to Legislative branch.

Labels: Federal Reserve

Wednesday, June 24, 2009

Reading two FOMC statements

- Now says "pace of contraction is slowing", a second derivative kind of assessment. Last time they qualified with contraction "appears to be somewhat slower."

- Sees progress in getting inventories under control relative to sales. (See this for data.) I don't see any other optimism in the statement relative to April than this.

- Recognizes that "prices of energy and other commodities have risen of late" but "substantial resource slack" means they still think inflation fears are "subdued". Anyone looking for statements about concern over future inflation will be disappointed by the middle paragraph.

- Actual policy is the same, both on the rate side and in terms of quantitative measures.

- Drops reference to "facilitating the extension of credit to households and businesses" that was in the April statement. Not sure whether this signals they are done with creating new facilities. The new statement concludes by saying that after monitoring its balance sheet it will "make adjustments to its credit and liquidity programs as warranted," which might be their signal that they are thinking about how to unwind their balance sheet expansion.

with price stability." That discussion might have moved the last sentence as indicated in my last bullet point. But the Fed isn't moving as fast as some would like. �If there was a surprise, then maybe it was the fact that there was no mention of the exit strategy,� said one trader as stock and bond markets reacted badly.

Labels: economics, Federal Reserve, money

Monday, June 22, 2009

Your interest rate stimulus is fading, fading, fading...

Chairman Ben S. Bernanke has to convince investors the Federal Reserve can take back more than $1 trillion it pumped into the U.S. banking system to pull the economy out of the longest decline in more than six decades.It doesn't help that the Treasury is pushing another $104 billion of supply into the bond market this week either. �Increased supply of bonds will of course push down bond prices and thus push up bond yields, carrying other interest rates with them.

...�The markets don�t understand the Fed�s exit strategy; they�re confused,� said Lyle Gramley, a senior economic adviser with New York-based Soleil Securities Corp. and former central- bank governor. �That�s contributed to the rise in long-term rates.�

The risk is that higher rates will hold back the budding economic recovery by lifting borrowing costs for homeowners and buyers. Economists surveyed by Bloomberg forecast growth of 0.5 percent in the third quarter after gross domestic product shrank for four consecutive quarters -- the first time that�s happened since 1947.

�It�s not good for the economy,� said Michael Feroli, a former Fed official who�s now an economist at JPMorgan Chase & Co. in New York. �It pushes back the housing rebound.�

The yield on the 10-year Treasury note ended trading at 3.78 percent June 19, up from 2.21 percent at the end 2008.

The average 30-year mortgage rate rose to 5.59 percent earlier this month, the highest since November, before slipping to 5.38 percent in the week ended June 18, according to Freddie Mac, the McLean, Virginia-based mortgage-finance company.

As soon as you introduce methods to deal with the crisis, as we did, that are out of the norm, you should very quickly begin to think about what your exit strategy is. And that is the process we are in right now and we're thinking it through...So this puts the Fed in a bit of a box this week. While tightening now is probably not in the cards, there may come a time they want to do so. �Failure to signal this week that the value of the dollar is a concern to them -- one they are willing to invest in -- will probably start the process of higher inflation. �Either higher nominal rates (through higher inflationary expectations) or higher real rates (in defense of the dollar) means the interest rate cycle has begun the process back up, which is bad news for housing.

We have put an enormous amount of liquidity into the system ... If it is allowed to remain indefinitely, and we keep a very low (interest) rate for an extended period of time, then we do risk an inflationary outbreak.

Labels: economics, Federal Reserve

Thursday, June 18, 2009

"We won't push it, but they're evil"

Labels: Federal Reserve

Wednesday, June 17, 2009

First look at bank reform -- not impressed

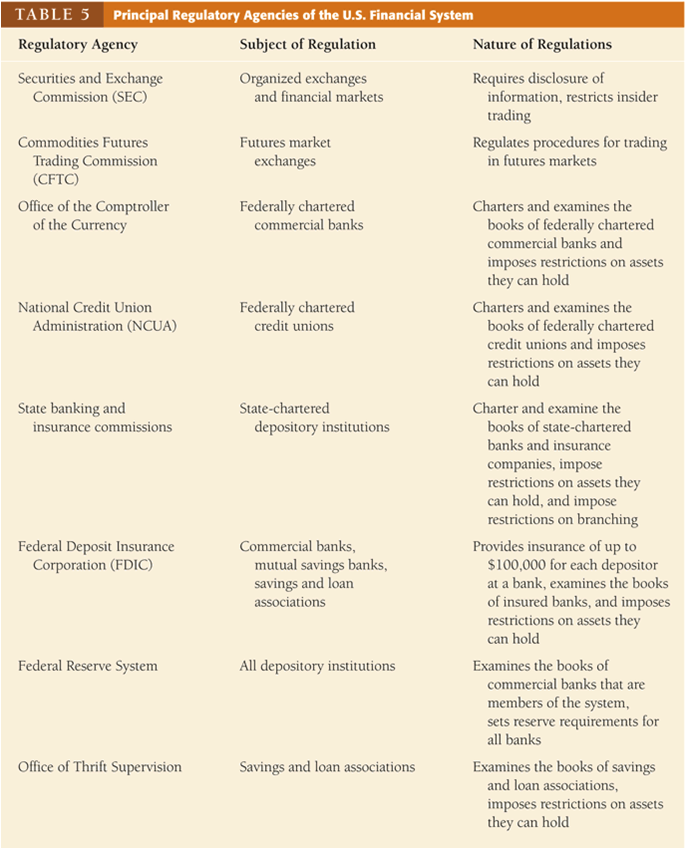

Above (please click to enlarge) is Table 5 from Chapter 2 of Frederic Mishkin's The Economics of Money, Banking and Financial Markets, 8th edition.* It maps for you the variety of regulators currently in the U.S. banking system. There's an interesting passage in the book much later on regarding multiple regulatory agencies:

Above (please click to enlarge) is Table 5 from Chapter 2 of Frederic Mishkin's The Economics of Money, Banking and Financial Markets, 8th edition.* It maps for you the variety of regulators currently in the U.S. banking system. There's an interesting passage in the book much later on regarding multiple regulatory agencies:Commercial bank regulation in the United States has developed into a crazy quilt of multiple regulatory agencies with overlapping jurisdictions. The Office of the Comptroller of the Currency has the primary supervisory responsibility for the 1,850 national banks which own more than half of the assets in the commercial banking system. The Federal Reserve and the state banking authorities have join primary responsibility for the 900 state banks that are members of the Federal Reserve System. The Fed also has regulatory responsibility over companies that own one or more banks (called "bank holding companies") and secondary responsibility for the national banks. The FDIC and the state banking authorities jointly supervise the 4,800 state banks that have FDIC insurance but are not members of the Federal Reserve System. The state banking authorities have sole jurisdiction over the fewer than 500 state banks without FDIC insurance. (Such banks hold less than 0.2% of the deposits in the commercial banking system.)That last bit is amusing (Mishkin has a new edition out next month, and I can't wait to see what he does with that second paragraph now!) So as we look at the new draft from the White House, what do we see? In their words (p. 2)

If you find the U.S. bank regulatory system confusing, imagine how confusing it is for the banks, which have to deal with multiple regulatory agencies. Several proposals have been raised by the U.S. Treasury to rectify this situation by centralizing the regulation of all depository institutions under one independent agency. However, none of these proposal has been successful in Congress, and whether there will be regulatory consolidation in the future is highly uncertain. (pp. 249-50)

- A new Financial Services Oversight Council of prudential regulators to identify emerging systemic risks and improve interagency cooperation.

- New authority for the Federal Reserve to supervise all firms that could pose a threat to financial stability, even those that do not own banks.

- Stronger capital and other prudential standards for all financial firms, and even higher standards for large, interconnected firms.

- A new National Bank Supervisor to supervise all federally chartered banks.

- Elimination of the federal thrift charter and other loopholes that allowed some depository institutions to avoid bank holding company regulation by the Federal Reserve.

- The registration of advisers of all hedge funds and other private pools of capital with the SEC.

It will take days to read and digest what's in there. For example, I'm quite concerned about the reduction in Federal Reserve independence that is reflected in the proposal (on p. 14) to force the Fed to get a signature from the Secretary of the Treasury before it could invoke its emergency powers (under Section 13(3) of the Federal Reserve Act) to prevent a financial crisis. I'm sure there are other little noxious nuggets among the 85 pages in this thing.

Let me make two points though. First, I showed the structure above and the quote from Mishkin to point out that most of us have thought the regulatory system was, if anything, too unwieldy. We were hoping for simplification. At first reading this proposal drops one regulator (the Office of Thrift Supervision, within FDIC) but puts two in its place, one for consumer finance protection and one for insurance firms. That just feels like it's going in the wrong direction, based on what we've taught in money and banking for the 25+ years I've done it.

Second, I fully agree with Arnold Kling that the Fed does see systemic fragility of the financial system as within its purview. I wrote several weeks ago that the Fed has basically two modes of conduct: in normal mode it fights inflation (with some eye on "high employment" as its goals insist -- the degree to which it looks at that varies by Fed chairman); in emergency mode it will act as a lender of last resort without regard to inflation in the short run. I am not yet sure there's any discussion in this draft of the connection between regulation and lending of last resort, or the connection between each of those and deposit insurance. (See Kahn and Santos [2005] for more.)

Kling also notes the Treasury brief is mute on housing policy. Can't imagine why.

*See also this from the Federal Reserve.

Labels: banking, economics, Federal Reserve, housing

Thursday, June 11, 2009

Regarding the Laffer spike

...we know that the payment of interest on bank reserves�which we have discussed in this forum many times (here and here, for example)�means a higher demand for reserves in the future than in the past. This change, of course, means that levels of the monetary base that would have seemed scary in the past will become the new normal. How big can the "new normal" be? That's a good question, and one I will continue to contemplate. But the assertion in the Laffer article that "a major contraction in monetary base" is required cannot be supported by either current evidence or simple economic theory.You currently get 0.25% on excess reserves, roughly what is paid on a six-month T-bill. Banks are holding more T-bills too, further indicating their desire for liquidity at present. I wrote three months ago:

We write about the wall of monetary base as if it is an excess supply of bank reserves; it's almost certainly not in the present environment. When it is, only then can it be inflationary.cf. the Banaian spike?

Labels: economics, Federal Reserve

Friday, May 29, 2009

Keep yer britches on: Nobody's replacing the dollar standard (yet)

Warning signs abound. Earlier this month, the Treasury discovered that demand had significantly decreased for its long-term bonds. In order to get buyers at its regular auction � the device by which the United States runs on deficit spending � it had to hike the interest rates it pays the bondholders. It signaled a lack of confidence in America's ability to sustain its debt expansion, which has the effect of worsening it through heavier debt service payments on the bonds they managed to sell.Now to be fair, Ed explains back on HotAir that "I allowed my imagination to run" and "I like to engage in a little speculative thinking," and that's great. I suppose I've done some of that on this blog. �But it's worth kicking the tires on this idea to understand what happened and why.

That reinforcing cycle of cascading debt has analysts worried enough to openly discuss downgrading U.S. debt. Financial Times reported this week that Standard and Poor has already done that for Great Britain's foreign debt, issuing a �negative� rating that will require more generous interest terms in order to sell bonds in international markets. The same kind of deficit spending in the United States will eventually trigger a re-evaluation of the U.S. credit, as the United States and United Kingdom face similar debt spirals with no end in sight.

Looking at the 12m change actually understates the swing in central bank demand. In the first quarter of 09, the outstanding stock of longer-term Treasuries rose by $278 billion. Central banks � according to the Treasury data � only bought $25 billion of longer-term Treasuries (all in March, and likely mostly short-term notes). China only bought $15 billion (all in March). Over that time period, central banks bought $85 billion in short-term Treasury bills, including $32 billion from China.

Labels: banking, economics, Federal Reserve