Tuesday, March 11, 2008

Two radios today

I'm on two internet radio programs today. At noon CT I will be on Midstream Radio with Jazz Shaw and the Lady Logician. They write to ask me to explain Paul Krugman's column from yesterday. Consider me sympathetic to it; more below. (Note: Those wanting graphs with their Krugman go here.)

At 2:30pm CT I will be joining Ed Morrissey with his new Ed Morrissey Show (part of his new duties at Hot Air). He wants to talk about Brad Schiller's article in the WSJ yesterday on the reporting of inequality. That deserves a separate post which will appear above this one.

Back to Krugman. A speech by New York Federal Reserve President Timothy Geithner has him worried. What got him worried? Here's a paragraph:

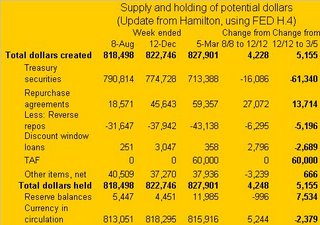

The Federal Reserve facing these liquidity issues -- and still faced with inflation higher than they would like -- has engaged in what James Hamilton calls monetary policy on the asset side of the balance sheet. In it Hamilton says the Fed's policy has rotated from its usual actions on monetary base -- the liability side of the Federal Reserve balance sheet -- to its asset side. I've updated his table to show what's happened since mid-December:

There hasn't been still much of a change in the monetary base -- there has been about a doubling of bank reserves, indicating that banks are laying away some money to protect themselves. When I wrote in August, the Fed was trying to use the discount window itself. The Fed has moved towards buying more and more assets through its term auction facility. It is permitting a variety of assets to be purchased through this, leading one writer to refer to the Fed as a pawnbroker as Krugman mentions. But those collateral are no different in type than they bought before -- it's just that they're more risky, and everyone knows it.

(UPDATE: I failed to mention yesterday's action expanding a second "Term Securities Lending Facility." This strikes me just as more of the same; Douglas Elmendorf shows that it's two transactions combined to one, both on the asset side. Remember what Bagehot said? Lending on "any good paper". Or Jeffrey Lacker in August said, one needs to make credit available without interfering with market assessment of risk. It's the destruction of credit that is to be avoided. Does the TSLF interfere with market assessment of risk? I don't yet see it.)

Where I "mostly agree" with Krugman -- the effect of these effects diminishes each time we try to add more reserves this way while we sterilize the the inflow of money. The Fed is selling off its Treasury holdings to absorb back the excess credit they are creating. In theory, we should not be generating additional inflationary pressures this way, and nothing in the money supply data would indicate to me a sharp increase in inflationary expectations. But they are nonetheless there, even if Bernanke doesn't seem too concerned.

As to Krugman's conclusion, that something must be done about the risks in mortgage markets, I wonder what he thought of George McGovern? I've looked at the change in risks by looking at the change in the spread between Baa and Aaa corporate bonds; it's risen, but only to levels that existed in 2003. That is not part of the anatomy of a crisis. I also wrote last August that asking banks to take an ownership position in houses -- an idea that seems not only to be not going away but being encouraged by people who should know better -- is a major risk to us getting out of the current jam. The market seems to be compelling banks to take their haircuts (in part by selling a piece of themselves to sovereign wealth funds, something Ed wants to talk about.) The political system is what is stopping homeowners from being told to do the same thing.

At 2:30pm CT I will be joining Ed Morrissey with his new Ed Morrissey Show (part of his new duties at Hot Air). He wants to talk about Brad Schiller's article in the WSJ yesterday on the reporting of inequality. That deserves a separate post which will appear above this one.

Back to Krugman. A speech by New York Federal Reserve President Timothy Geithner has him worried. What got him worried? Here's a paragraph:

The current episode has a basic dynamic in common with all past crises. As market participants have moved to reduce exposure to further losses, to step on the brake, the brake became the accelerator, amplifying the shock. Measured risk has increased more quickly than many institutions have been able reduce it, and attempts to reduce it have added to volatility and downward pressure on prices, further increasing measured exposure to risk. Uncertainty about the market value of securities and about counterparty credit risk has increased, and many hedges have not performed as intended. The rational actions taken by even the strongest financial institutions to reduce exposure to future losses have caused significant collateral damage to market functioning. This, in turn, has intensified the liquidity problems for a wide range of bank and nonbank financial institutions.In English, then: Everyone tried to get out of their positions at once, and put downward pressure on prices of the assets they were holding. I had two people quote a statistic today to me while I was off-campus (and an international visitor on-campus) that 10% of mortgages today are worth more than the houses that are their collateral. The damage has spread even to hedge funds backed by Treasuries, which almost never happens: Treasuries are supposed to be safest of the safe. Now that's collateral damage.

The Federal Reserve facing these liquidity issues -- and still faced with inflation higher than they would like -- has engaged in what James Hamilton calls monetary policy on the asset side of the balance sheet. In it Hamilton says the Fed's policy has rotated from its usual actions on monetary base -- the liability side of the Federal Reserve balance sheet -- to its asset side. I've updated his table to show what's happened since mid-December:

There hasn't been still much of a change in the monetary base -- there has been about a doubling of bank reserves, indicating that banks are laying away some money to protect themselves. When I wrote in August, the Fed was trying to use the discount window itself. The Fed has moved towards buying more and more assets through its term auction facility. It is permitting a variety of assets to be purchased through this, leading one writer to refer to the Fed as a pawnbroker as Krugman mentions. But those collateral are no different in type than they bought before -- it's just that they're more risky, and everyone knows it.

(UPDATE: I failed to mention yesterday's action expanding a second "Term Securities Lending Facility." This strikes me just as more of the same; Douglas Elmendorf shows that it's two transactions combined to one, both on the asset side. Remember what Bagehot said? Lending on "any good paper". Or Jeffrey Lacker in August said, one needs to make credit available without interfering with market assessment of risk. It's the destruction of credit that is to be avoided. Does the TSLF interfere with market assessment of risk? I don't yet see it.)

Where I "mostly agree" with Krugman -- the effect of these effects diminishes each time we try to add more reserves this way while we sterilize the the inflow of money. The Fed is selling off its Treasury holdings to absorb back the excess credit they are creating. In theory, we should not be generating additional inflationary pressures this way, and nothing in the money supply data would indicate to me a sharp increase in inflationary expectations. But they are nonetheless there, even if Bernanke doesn't seem too concerned.

As to Krugman's conclusion, that something must be done about the risks in mortgage markets, I wonder what he thought of George McGovern? I've looked at the change in risks by looking at the change in the spread between Baa and Aaa corporate bonds; it's risen, but only to levels that existed in 2003. That is not part of the anatomy of a crisis. I also wrote last August that asking banks to take an ownership position in houses -- an idea that seems not only to be not going away but being encouraged by people who should know better -- is a major risk to us getting out of the current jam. The market seems to be compelling banks to take their haircuts (in part by selling a piece of themselves to sovereign wealth funds, something Ed wants to talk about.) The political system is what is stopping homeowners from being told to do the same thing.

Labels: economics, Federal Reserve, Media