Monday, January 14, 2008

Bonds and bridges on steroids

Governor Pawlenty's bond proposal came out this morning, and the St. Cloud Times headlines what is not in the bond:

Governor Pawlenty's bond proposal came out this morning, and the St. Cloud Times headlines what is not in the bond:It does not include requested state dollars to expand the St. Cloud Civic Center or to remodel and expand the National Hockey Center at St. Cloud State......two major projects local leaders have had on their minds for quite some time. How long until we hear Sen. "No-no-no", who has in the past pumped for more for the hockey center, has another fit about Governor Pawlenty's thrifty ways?

SCSU is proposed for money for Brown Hall, an old classroom building that has laboratories as old as me. (Rep. Steve Gottwalt told me about touring the facility and the faces of the legislators as they walked through; I think they keep one lab particularly antiquated and nasty-looking for the tour.) In the note from the faculty union reporting this to us, the lobbyist noted,

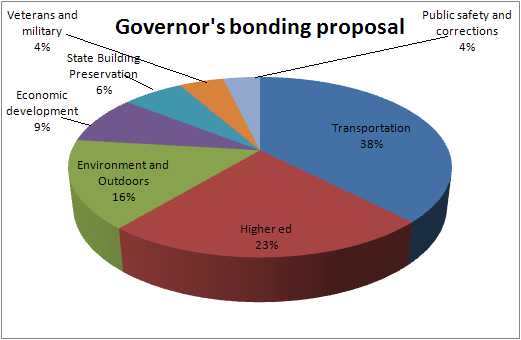

Concern over neglected transportation infrastructure is causing transportation funding to squeeze other segments of the capital investment bill. This means we have a stake in the outcome of the gas tax debate�if roads and bridges are funded out of a gas tax increase it would mean more bonding authority would be left over for projects such as higher education projects.I wanted to emphasize this point: The gas tax for funding transportation is not used instead of bonds (or in the slang used by DFL legislators, "the credit card") but in addition to bonds. We will pay just as much interest either way -- we'll just have less private investment increasing productivity with which we pay off those bonds with our future taxes. The gas tax makes government bigger; the discussion of the means of funding is just smoke. And it is highly unlikely the Legislature adjourns and the House goes to the voters without a bunch of money spent on bridges; the demand is still there.

There's plenty not to like about the governor's bond request -- I might start with $70 million more down the Central Corridor rat-hole -- but funding of bridges through bonding is certainly something to like. The "benefit principle" of public finance says that the people receiving the most benefit from a public good should be the ones that pay. That's one reason why we ask people to pay fees to enter state parks, for example. The alternative principle is "ability to pay." But in either case bonding can be the preferred option. Bridges last 30-40 years or more, and there is no reason why we should expect the current taxpayers to fund the driving of individuals using the bridge a generation from now; bonding assures that those driving the bridges are paying for them. And if investments in infrastructure like bridges are to increase state productivity, then the income of future generations will be higher than those in the present. If it is enough higher, the tax burden will be lighter on future than current generations, again arguing that some of the cost be shifted forward. Under any reasonable assumptions about the value of future Minnesotans' utility or satisfaction versus the value of present Minnesotans' utility, it is good public policy to use bonding. (Of course this may be controversial, as we've been arguing for some time over the rate of discount of future generations in the global warming debate. You'd have to work the math a bit to convince me it matters here.)

Now part of the problem, in my view, stems from what appears to be a formula that translates the size of the state budget to the size of the bonding proposal (which would put the amount planned here at about 3% of the biennial budget.) I had Rep. Larry Haws while I guest-hosted on the KNSI Morning Show a couple of weeks ago in which he made some reference to this; about the only sense I could make of this -- assuming there is some formula they use -- is that it keeps the rating agencies happy so that the interest cost of debt stays predictable. But one could easily imagine that cost-benefit analysis could be applied to the bridges to argue for an amount of bonding above this formula, as long as the return on investment was sufficient to cover the opportunity costs. Much like Nixon-to-China, it may be up to the DFL to come up with a way to use cost-benefit judiciously to make the case for a larger bond.

UPDATE: Lileks wonders about light rail. See moreover this from the LA Times (h/t: Peter Gordon):

Paradoxically, the MTA's rail projects, which required fare increases and reduced bus services, have cost the transit system riders. Using MTA data, our analysis indicates that they produced a drop in train and bus ridership of more than 3 billion boardings from 1986 to 2007.

Although we've now gotten back to 1985 levels in terms of public-transit use, the county population has grown by more than 2 million since then. That means, on a trip-per-capita basis, the transit system is still not performing -- by 20% -- as well as it did 22 years ago.

Labels: cost-benefit analysis, economics, legislature, Minnesota, Pawlenty