Friday, May 22, 2009

There may be more trickle down

Bloomberg reports on the trickle-down of Bear Stearns.

Bloomberg reports on the trickle-down of Bear Stearns. Cavonberry�s, Yang�s 46th Street shop near the headquarters of the New York firm taken over by JPMorgan Chase & Co., once bustled with finance workers jostling to buy a barbeque chicken chopped salad and bottled water for $12. �They used to be turning them away at the door,� Irace said.Says one person in the story, "�The higher your income, the more in services you consume. You don�t iron your own shirt.� But what if some of that income is coming from reasons other than one's own skill? Philippon's research shows for example that maybe half of the wage premium in financial services was due to deregulation (greater returns to skill in exploiting a more risky environment), so that the share of financial services in GDP rose more than expected by historical experience. He argues that roughly 700,000 jobs needed to be lost in insurance and finance to get back to those levels. The data in the graph above are not strictly comparable because they include real estate, which Philippon doesn't seem to include.

Last week, slow enough that one cashier instead of the usual two operated the register at midday, Yang tallied up the ripple effect of the financial slump that cost Bear Stearns its independence: He negotiated a $4,000 monthly decrease in rent with Sierra Realty Corp., to $17,000, and is spending 35 percent less a week with Fischer Foods of New York Inc. for such things as artichokes and ham.

�Since January, everything�s dead,� said Yang, 52.

The biggest Wall Street crisis since the Great Depression isn�t just a setback for New York or bankers. The finance industry�s contraction may wipe out $185 billion in wages and profits, or $600 for every man, woman and child in the U.S., according to Thomas Philippon, a finance professor at New York University�s Stern School of Business. The trail of reduced income affects car mechanics, waiters, sports teams, hair stylists, jewelers, housecleaners and watch repair shops.

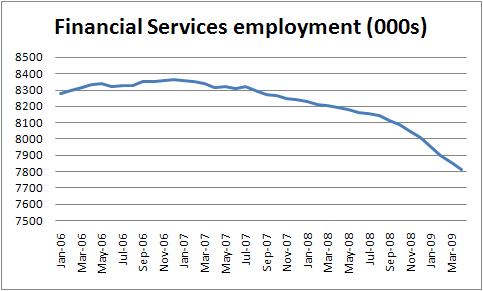

My colleague Rich MacDonald and I have puzzled over this for awhile: How is it that the bottom seems to fall out of finance, and yet only 5% of jobs in the area have been lost from the Dec 2007 peak in the business cycle? Based on what I see in the BLS data, insurance employment has not even fallen 50,000, and the Bloomberg article puts finance job losses at about 250,000. So we have a ways to go to get back to a 2001-level financial world, at least in terms of employment.

Labels: economics