Thursday, March 13, 2008

Two for two, two to go

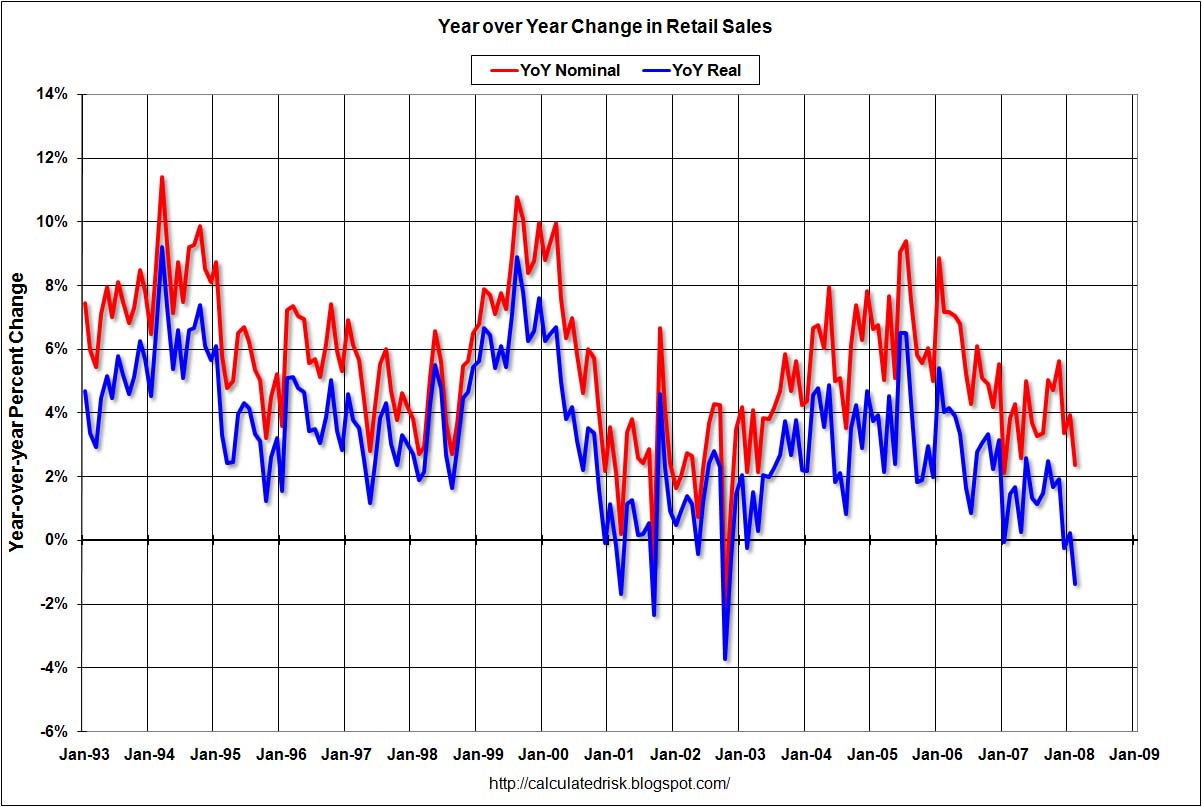

The second shoe of the recession has started brigade fell this morning, as retail sales surprised us with a -0.6% reading versus a +0.1% expectation. The year-over-year level of real retail sales graphed on the blue line to your left (courtesy Calculated Risk) has fallen below zero now for two of the last three months. While many want now to say "the recession has started", I'm going with the view that it started last December (about which I speculated two months ago.)

The second shoe of the recession has started brigade fell this morning, as retail sales surprised us with a -0.6% reading versus a +0.1% expectation. The year-over-year level of real retail sales graphed on the blue line to your left (courtesy Calculated Risk) has fallen below zero now for two of the last three months. While many want now to say "the recession has started", I'm going with the view that it started last December (about which I speculated two months ago.) I will note that the UCLA forecast is just out, saying no recession. I think it's reasonable for disagreement still to exist and my earlier skepticism regarding the call of a recession in Minnesota is a conservatism in announcements that most economists share, I believe. But I'm now looking at graphs for employment and real sales, both of which are heading down (that WSJ economist survey now has 2008 job growth averaging a wretched 9,000 per month). We won't get the other two broad indicators for February until industrial production (Monday) and personal income (the 28th), but I doubt they are going to give us anything different than the world William Poole is describing.

Fed policy is always properly described as sort of walking a tightrope, trying to balance the various policy objectives. The problem is in today's situation, that tightrope is really being shaken hard. � The objectives (are) inflation control and of full employment. (It's) market instability that is shaking the tightrope.And intriguingly the response is to act as the "fool of last resort". The question seems to be whether this is going to be something that the Federal Reserve can do with inflation being held under control, or whether the liquidity implied in these lending facilities cannot be mopped by offsetting Fed transactions? Steve Waldman is skeptical, John Palmer says it's not a good idea, and Ken Rogoff calls the United States "ground zero for global inflation." (h/t: Mankiw)

Labels: economics