Monday, October 03, 2005

Supply is a schedule

I like the low-hanging fruit principle that Phil Miller evinces talking about oil.

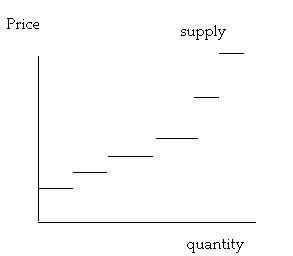

You typically draw them as smooth upward or downward sloping curves, but they may look much more like this staircase. At each step, you've exhausted the apples on the branch, or the oil under pressure. As the price rises, more expensive forms of extraction become profitable. If the price rises over $100 a barrel for oil, maybe solar panels for your home heating become viable. At $120, battery-powered cars that can do 70 mph on the highway are feasible, feasibility meaning not just technically possible, but economically efficient -- someone can be compensated fully for the costs of production.

You typically draw them as smooth upward or downward sloping curves, but they may look much more like this staircase. At each step, you've exhausted the apples on the branch, or the oil under pressure. As the price rises, more expensive forms of extraction become profitable. If the price rises over $100 a barrel for oil, maybe solar panels for your home heating become viable. At $120, battery-powered cars that can do 70 mph on the highway are feasible, feasibility meaning not just technically possible, but economically efficient -- someone can be compensated fully for the costs of production.

The area under any supply curve represents the opportunity cost of production to a producer. Costs are always costs to someone. The reason we pick the low-hanging fruit is because it's economical.

Assuming all apples on a tree are of equal quality, when someone picks an apple, she picks an apple that requires the least amount of effort (has the lowest cost). Subsequent apples "cost" more to acquire. To give firms and incentive to produce more, they must receive additional compensation.Everyone says to be an economist you only need to teach a parrot to say "supply and demand", but few understand what lies behind each. They are schedules, indicating at each price how much producers will supply or how much consumers will demand.

The principle works with oil too. John Palmer and John Chilton point us to this Fortune Magazine article about the Tar Sands of Alberta.

You typically draw them as smooth upward or downward sloping curves, but they may look much more like this staircase. At each step, you've exhausted the apples on the branch, or the oil under pressure. As the price rises, more expensive forms of extraction become profitable. If the price rises over $100 a barrel for oil, maybe solar panels for your home heating become viable. At $120, battery-powered cars that can do 70 mph on the highway are feasible, feasibility meaning not just technically possible, but economically efficient -- someone can be compensated fully for the costs of production.

You typically draw them as smooth upward or downward sloping curves, but they may look much more like this staircase. At each step, you've exhausted the apples on the branch, or the oil under pressure. As the price rises, more expensive forms of extraction become profitable. If the price rises over $100 a barrel for oil, maybe solar panels for your home heating become viable. At $120, battery-powered cars that can do 70 mph on the highway are feasible, feasibility meaning not just technically possible, but economically efficient -- someone can be compensated fully for the costs of production.The area under any supply curve represents the opportunity cost of production to a producer. Costs are always costs to someone. The reason we pick the low-hanging fruit is because it's economical.