Monday, June 04, 2007

What if you choose well and are still poor?

I was reading Mitch's poverty riff over the weekend and thought again to myself how often we miss the point of poverty by making bad calculations. Mitch spends the early part of his post describing how little money he had while making choices of how to live his life in order to invest in his human capital:

Prudence is, well, prudent. She invests in her education or in some skills, perhaps to become a world-class artist, athlete, chef or talk radio personality. She accepts the lower income of her early years in return for a peak period later on. (You might wish to argue that income should be replaced with satisfaction -- I don't think Mitch ever planned to get rich in radio but he loves the activity, as anyone who's sat in a broadcast with him can attest.) That job can generate enough income for her later on to make it worthwhile to forgo the amount of income Jimmy makes.

Jimmy is not necessarily a spendthrift, but he has made the choice to forgo some of his investment in human capital in order to consume a higher income stream now. He then has a lower rate of appreciation of his income over his lifetime. They both decline as they approach death (that's the place where the line goes to zero, assumed to happen simultaneously for these two) and we've no reason to think one can invest for retirement better than the other. You can change the assumptions if you want, but these wouldn't change my basic point.

You hear sometimes that people "made choices" that make them poor. Here you can see that Prudence makes a choice that makes her poorer than Jimmy for quite some time. Perhaps the poverty level is set between their two income levels in their youth. My point is that if poverty is measured on a year-to-year basis, as many of Mitch's commenters did, you end up calling Mitch poor or not poor at some point in time in his past, and that misses the point of what he was doing. He's engaged instead in human capital investment. My students often do this too, by delaying graduation so they can work part time and take a lesser course load, or by coming back to school and quitting their jobs for awhile.

This struck me again when I was reading a high school senior's commencement address in the paper this morning.

Or, as Mitch puts it:

It's not enough to tell people to "go for the gold" -- they have to know what gold is.

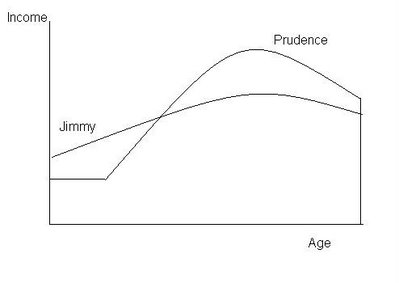

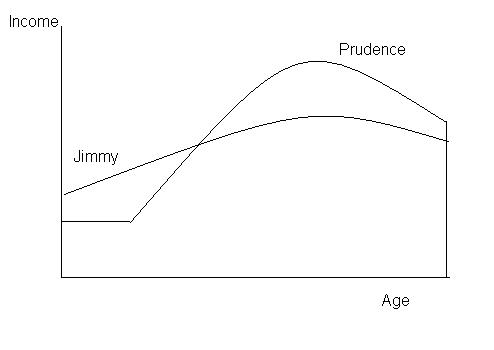

I was choosing, at the time (and it turned out to be a bad choice) to sacrifice a lot, one might say even obsessively, to try to re-jumpstart my radio �career�...Now that stuck in my head a day or two, because you wonder how many people make "bad career choices" and end up poor. We know of the investments in good human capital. I often draw a graph below to describe the differences between Prudence and Jimmy. (This is a pretty common diagram to draw in getting intermediate macro students to understand lifetime savings, income and consumption. I get the suspicion I've drawn this graph for you before, dear reader, but I can't find it in my archives right now.)

Prudence is, well, prudent. She invests in her education or in some skills, perhaps to become a world-class artist, athlete, chef or talk radio personality. She accepts the lower income of her early years in return for a peak period later on. (You might wish to argue that income should be replaced with satisfaction -- I don't think Mitch ever planned to get rich in radio but he loves the activity, as anyone who's sat in a broadcast with him can attest.) That job can generate enough income for her later on to make it worthwhile to forgo the amount of income Jimmy makes.

Jimmy is not necessarily a spendthrift, but he has made the choice to forgo some of his investment in human capital in order to consume a higher income stream now. He then has a lower rate of appreciation of his income over his lifetime. They both decline as they approach death (that's the place where the line goes to zero, assumed to happen simultaneously for these two) and we've no reason to think one can invest for retirement better than the other. You can change the assumptions if you want, but these wouldn't change my basic point.

You hear sometimes that people "made choices" that make them poor. Here you can see that Prudence makes a choice that makes her poorer than Jimmy for quite some time. Perhaps the poverty level is set between their two income levels in their youth. My point is that if poverty is measured on a year-to-year basis, as many of Mitch's commenters did, you end up calling Mitch poor or not poor at some point in time in his past, and that misses the point of what he was doing. He's engaged instead in human capital investment. My students often do this too, by delaying graduation so they can work part time and take a lesser course load, or by coming back to school and quitting their jobs for awhile.

This struck me again when I was reading a high school senior's commencement address in the paper this morning.

The first thing I want to tell you is this: If you have lofty goals, go after them now, while you can. If you want to be an Olympic skier, do it ...! If you want to pursue a career in blues guitar, do it ...! If you want to save the world, do it ...!(I deleted the names of the three students he addressed. Maybe they don't want to be here.)

Right, but what if you make those choices and they turn out to be "bad choices"? If your choices land you "in poverty", what is to be done? We have some answers to offer in economics. We know that if we compensate those who take risks and made "bad choices" but we tax those who take risks and made "good choices", the resulting behavior is to encourage risktaking without careful consideration of whether what your going for the gold has value to society. And if we let the losses stand and subsidize the winners, everyone tries to do the same thing and risktaking is discouraged. People respond to incentives.If you can offer something to society � no matter how seemingly small it may be � you matter, you are an integral part of our community and society.

So, if you want to "go for the gold," figuratively or literally, do it. No one here will stop you.

Or, as Mitch puts it:

If society is going to subsidize anything, it should be good behavior - staying in school, learning a skill that can eventually help someone support themselves and those for whom they�re responsible, putting down the damn bong and keeping your johnson in your pants and learning how to support oneself and, eventually, raise families that value the same thing.

It's not enough to tell people to "go for the gold" -- they have to know what gold is.

Labels: economics, education, NARN